Coronavirus scare dominates, Worst week for five months, BoC dovish

Mon Jan 20

US markets were closed today, and volatility was light elsewhere, with DAX making small gains, but FTSE and GBP falling on remarks by the UK Chancellor Javid that the UK would not adhere to EU standards after leaving next week. Forex was also fairly quiet, a small move up in CAD led to a flat dollar overall. Gold and Bonds were slightly up, and Oil was down, following the UK mood.

Tuesday January 21

Asian markets fell on the Chinese coronavirus scare, and this mood was reflected in Europe and the US, with all markets down, although a late recovery meant SPX was flat, and NDX up. Nevertheless, DAX briefly hit an all-time high before pulling back. Positive results after hours for NFLX and IBM helped. GBP recovered and rose but otherwise currencies were down. The only exception was JPY, which along with Bonds and Gold was up, in line with the equity risk-off move. Oil was down for the same reason.

Wednesday January 22

SPX and NDX recovered at first today, briefly making intraday all-time highs, but fell back along with other markets as the virus scare dampened enthusiasm. Haven assets Gold and Bonds were up, although JPY was flat. A sharp early rise in GBP, followed the PSBR beat at 0930, and an expectation that interest rates will not be cut. CAD fell 1% on a dovish BoC report, downgrading growth projections. With EUR slightly up, the CAD move was not enough to prevent DXY from posting a red candle for the day.

Thursday January 23

Stocks fell again in early trading but rebounded on a WHO report that the coronavirus was not “a global emergency”, and all except FTSE closed up. A sharp fall in EUR after a dovish (or at least not hawkish, as expected) ECB presser resulted in a sharp uptick in DXY. AUD was strongly up on the Australian jobs beat, but gave up all up in the US session, on virus fears. The late rebound was not enough to prevent the haven trio from rising across the board, and Oil falling again.

Friday January 24

A second coronavirus case in the US caused a huge plunge in SPX, down 1% from the high of day, after an early rally. European indices did not therefore join in, and although pulling back slightly from the highs of the day, DAX and FTSE still closed green. Like yesterday, NKY was down on further yen strength. The dollar, however was up overall due to continuing EUR weakness, and a pullback in GBP. The haven trio of Gold, Bonds and JPY were all up, and Oil was down, in line with the equity move.

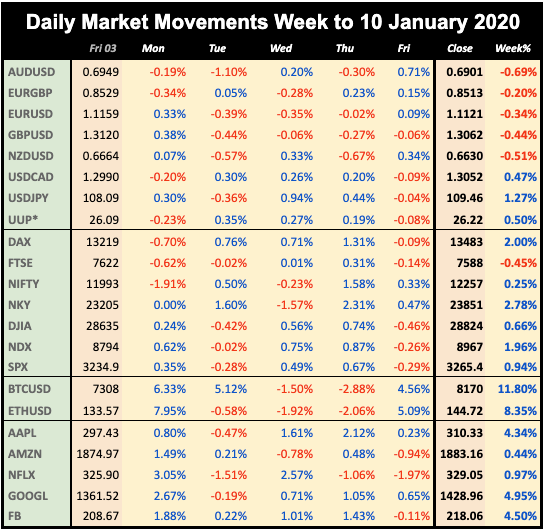

WEEKLY PRICE MOVEMENT

Equities were down with the worst performer DJIA hit as proportionally more earnings releases added to the downward sentiment. AUDJPY was the strongest mover, down 1.61%. FANGS held up quite well, with NFLX earnings bucking the trend and adding 3.97% to the TV giant. Cryptos pulled back after last week's rally but volatility is still quiet.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- US and UK Rate Decisions

- Chinese New Year

- AAPL AMZN MSFT Earnings

- UK leaves the EU

Monday January 27

Markets are closed in China, Hong Kong, Taiwan and Vietnam for the Chinese New Year. The last Year of the Rat was 2008! Australia and Korea are also closed. This week, watch out for movement in the Democratic primary candidates support ahead of the Feb 3 caucus (Biden: good for markets, Sanders and Warren: less so). The Italian regional election on Sunday may affect European markets.

09:00 EUR Germany IFO Climate/Expectations (Jan)

15:00 USD New Home Sales (MoM) (Dec)

Tuesday January 28

Earnings season continues with Dow defensive MMM before the bell, but the big one is AAPL, the world’s largest company (12% of NDX, 7.4% of DJIA and 4.84% of SPX) which joins fellow NDX stocks AMD and SBUX after the close. There is a rate decision today on HUF. Chinese markets remain closed until Friday.

13:30 USD US ND Capital Goods (MoM e0.2% p0.1%)

14:00 USD US S&P/Case-Shiller Home Price Indices

15:00 USD US Consumer Confidence

21:30 AAPL earnings

Wednesday January 29

The Fed rate decision today has a 1.75% hold 87% priced in, with a 13% possibility of a 25bp hike. A hold therefore points to a further upside in stocks. It’s another important earnings day today, with BA, DOW and MCD reporting pre-market. BA has been overtaken by AAPL as the top DJIA company, but is still 7.39% of the index, and the three together are 13.52% by weight. The end of the day sees MSFT FB and TSLA report. These three are 7.24% of NDX. All this portends a lot of volatility. Markets are closed in Mexico and New Zealand.

00:30 AUD Australia CPI (RMA Trimmed Mean QoQ e0.4% p0.4%)

07:00 EUR Germany Gfk Consumer Confidence Survey (Feb)

15:00 USD US Pending Home Sales (MoM) (Dec)

19:00 USD Fed Rate Decision/Statement (e1.75% hold)

19:30 USD FOMC Presser

21:45 NZD NZ Imports/Exports/TB

Thursday January 30

Today’s earnings are DJIA stalwart KO before the bell, and NDX giant (7.83% by weight) AMZN after the close. ECB hawk Wiedmann speaks at 1800.

08:55 EUR Germany UnEmp Rate/Change

10:00 EUR Eurozone UnEmp/Business Climate

12:00 GBP BoE Rate Decision/Statement

12:30 GBP BoE Presser

13:00 EUR Germany Prelim CPI (YoY e1.7% p1.5%)

13:30 USD US Prelim 19Q4 GDP (YoY e2.1% p2.1%)

13:30 USD US Jobless Claims/PCE QoQ)

23:30 JPY Tokyo CPI (Core YoY e0.8% p0.8%)

Friday January 31

Today is month end, which could involve repositioning, and also Brexit day, the long-awaited departure of Britain from the EU takes effect at 2300 (midnight in Europe). The Eurozone double GDP and inflation print is the most important event of the day.

02:00 CNY China PMIs

10:00 EUR Eurozone Prelim 19Q4 GDP (YoY e1.1% p1.2%)

10:00 EUR Eurozone Prelim CPI (Core YoY e1.4% p1.3%)

13:30 USD US PCE MoM/YoY

13:30 USD US Personal Income/Spending

14:45 USD Chicago PMI

15:00 USD Michigan CSI

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.