Possible delisting of China stocks, Talk of impeachment, UK prorogation cancelled

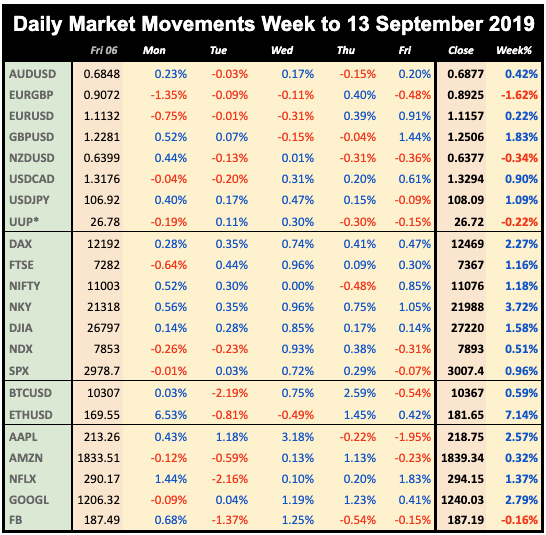

Indices were mixed today. SPX recovered from its knee-jerk fall after Friday’s Fed comments and China meeting cancellation to end the day flat. There was some difference of opinion about that event, as shown in a poll I created.

DAX and NKY were down, the former after another German Manufacturing PMI miss, but as GBP was strong, FTSE as always lagged. The currency picture was mixed with DXY adding 0.15% purely on EUR slippage, the other currencies were up as was Gold. Oil slipped slightly and yields were flat.

DAX and NKY were down, the former after another German Manufacturing PMI miss, but as GBP was strong, FTSE as always lagged. The currency picture was mixed with DXY adding 0.15% purely on EUR slippage, the other currencies were up as was Gold. Oil slipped slightly and yields were flat.

Tuesday September 24

US indices and Japan fell hard today, down 1% on possible Trump malfeasance with the Ukrainian president, raising the spectre of impeachment. In the UK, the prorogation of parliament was ruled illegal, a blow to the hard Brexit strategy and GBP rallied. FTSE gapped down, recovered, but ended the day lower. DAX on the other hand had a good day. DXY was down with all currencies and Gold advancing, particularly JPY. Yields and Oil were also down in line with risk-off.

Wednesday September 25

Hopes of fresh trade talks, and Trump ‘coming clean’ on the Ukraine matter halted the slide and SPX posted a 0.6% gain. NKY followed suit as JPY reversed back down. FTSE was once again down on GBP strength. Risk-on was seen more outside equities than within, with DXY up 0.67% and all currencies, Gold and Bonds down. Gold fell particularly sharply. Oil and DAX were however down on the day.

Thursday September 26

The see-saw continued today, with SPX and NKY down but DAX and FTSE up. The dollar was a little more certain, up across the board slightly, but Gold and Oil were flat. However yields climbed again. The US-Japan partial trade deal I referred to in last week was signed, but was overshadowed by talk from House Leader Nancy Pelosi about impeachment for the Ukraine issue, which the Republicans are calling Bidengate and the Democrats Ukrainegate.

Friday September 27

There was a sense of déjà vu today. My report last Friday started “Equities were doing moderately well on Friday until the afternoon session when it was revealed….” and so it was today. The White House said they were looking at controls on capital outflow to China, which in effect means Chinese companies such as BABA or BIDU would be unable to list in the US. SPX dropped 0.73% in four minutes and continued down, ending 0.5% in the red. NKY and Oil followed suit. The DAX pullback was much smaller, and FTSE ignored the whole thing (and a GBP slide) with a very flat day.

The dollar was fairly quiet through all this, fading a mere 0.08% as EUR recovered slightly after falling all week. If anything, the currency reaction was still risk-on, with advances in CAD and AUD, and declines in Gold, JPY and Bonds.

WEEKLY PRICE MOVEMENT

A definite difference between the US and rest of the world this week. The largest mover was NIFTY, still benefiting from the Indian tax cuts. The biggest forex move was GBPCAD down 1.55%. Cryptos fell hard, as did FANG stocks, FB faring worst.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- EU tariff announcement

- Fourteen PMI reports

- RBA rate cut expected

- Non-farm Payrolls

Monday September 30

The WTO ruling on Airbus subsidies is due today with tariff recommendations, which will cover other EU imports. The first two of 14 PMI reports this week are today. Expect the impeachment and trade dramas to carry on running. The end of the month and quarter may result in increased volatility.

23:50 JPY Japan Retail Sales (Sunday)

01:45 CNY China Caixin Manuf PMI (e50.2 p50.4)

06:00 EUR Germany Retail Sales

07:55 EUR Germany Unemployment Rate

08:30 GBP UK 19Q2 Final GDP (QoQ e0.5% p-0.2%)

09:00 EUR Eurozone Unemployment Rate

12:00 EUR Germany CPI (YoY e1.2% p1.0%)

13:45 USD Chicago PMI

23:30 JPY Japan Jobs/Unemployment

23:50 JPY Tankan Manufacturing Index/Outlook

Tuesday October 01

A new month and the first day of Q4. The ISM Manufacturing PMI is interesting, as the estimate brings it back into positive territory. PMIs are a good barometer of the effect of the trade war. A miss will not help markets. Plenty of Fed speakers on the roster. Markets are closed in China today for the rest of the week.

04:30 AUD RBA Rate Decision/Statement (e0.75% p1.00%)

07:55 EUR Germany Markit Manuf PMI

08:30 GBP UK Markit Manuf PMI

09:00 EUR Eurozone Prelim CPI (Core YoY e1.0% p1.0%)

09:20 AUD RBA Governor Lowe speech

12:30 CAD Canada GDP MoM

12:50 USD Fed Clarida speech

13:15 USD Fed Bullard speech

13:30 CAD Markit Manuf PMI

13:30 USD Fed Bowman speech

13:45 USD Markit Manuf PMI

14:00 USD ISM Manuf PMI (e50.0 p49.1)

Wednesday October 02

For once the quietest day of the week, with only the ADP (NFP ‘preview’) of interest. There is a rate decision on PLN (hold expected). Markets are closed in India.

08:30 GBP Markit Construction PMI

12:15 USD ADP Employment Change (e140k p195k)

14:50 USD Fed Williams speech

Thursday October 03

All PMIs today, although the profile will have been set earlier in the week. KO competitor PEP, unusually an NDX component has an August quarter-end, and reports today before the bell. Markets are closed in Germany and Korea.

01:30 AUD Aus I/E/Trade Balance

07:55 EUR Germany Markit Composite PMI

08:00 EUR Eurozone Markit Composite PMI

08:30 GBP UK Markit Services PMI

09:00 EUR Retail Sales (YoY)

12:30 USD Fed Quarles speech

12:30 USD Jobless Claims

13:45 USD Markit Services/Composite PMI

14:00 USD ISM Non-Manuf PMI (e55.0 p56.4)

14:00 GBP BoE Tenreyro speech

22:35 USD Fed Clarida speech

Friday October 04

NFP is the main story today, as always, and there is little else to distract. Note the Canadian report is next week. There is a rate decision on INR (25bp cut expected).

01:30 AUD Australia Retail Sales

12:30 USD US NFP/AHE/Unemp (NFP e140k p130k)

12:30 USD US Trade Balance

12:30 USD Fed Rosengren speech

12:30 CAD International Merchandise Trade

14:00 CAD Ivey PMI

18:00 USD Fed Chair Powell speech

I am hoping to pass 60,000 page views on the blog this weekend

I am hoping to pass 60,000 page views on the blog this weekend

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.