Mixed earnings, ECB less dovish than expected, British PM Johnson hawkish on Brexit

Mon Jul 22

After Friday’s dip markets were back up today on rate cut and earnings hopes.

Energy stocks were strong following a rise in Oil (and Gold) after Iran seized a British tanker in the Gulf in retaliation for their ship held in Gibraltar.

The mood was shared by USD (DXY +0.22%), as sentiment moved to only a 25bp rather than 50bp cut next week. Currencies were all down, but yields were flat.

Tuesday July 23

Strong earnings from KO and UTX set the mood for another green day on indices and Oil. Similarly USD continued to rise (DXY +0.42%), with EUR falling harder than most, on ECB dovishness expectations, and of course not helped by Brexiteer Boris Johnson being confirmed as Britain’s new Prime Minister. GBP suffered even more with EURGBP down 0.22%. All currencies and Gold were down in line, and yields rose 2bp on stock/bond rotation and dollar strength.

Wednesday July 24

A third day of earnings produced a marked divergence between DJIA and SPX. The former was down 0.3%, caused by disappointing earnings from CAT and BA, together 12% of the index. SPX however added 0.5% to close at another ATH. In currencies, a ‘Boris bounce’ (or maybe technical support) added 0.38% to GBP. With EUR further declining after the German Manufacturing PMI missed again, the dollar ended flat on the day. Yields and Oil both gave up yesterday’s advance, despite the EIA stock beat at 1430.

Thursday July 25

Equity markets came off today, after disappointing results from TSLA last night, and also AAL, warning of 737Max issues. AAL fell 8.4%, and BA fell a further 4%. The other trigger was the Durable/Capital Goods print (which ironically excludes aviation), which beat estimates. This was seen in a strong USDJPY (+0.44%) and 10-year yields (instant 8bp spike).

The ECB did not detail new stimulus to counter poor growth, and as markets were primed for dovishness, the net result was a spike up, and EUR closed up on the day, enough to trim DXY’s gain to 0.11%. (Note that DAX reacted instantly to this and the US Durables print). Elsewhere the Boris Bounce became a ‘Pfeffel Fade’ (Johnson’s third forename is de Pfeffel) as sterling returned to Tuesday’s level. Other currencies and Gold were also down, and Oil recovered somewhat.

Friday July 26

Strong earnings from GOOGL late Thursday and MCD set the pace for another advance in equities with new all-time highs, helped by the (preliminary) US Q2 GDP beat (2.1% v 1.8%) and PCE Q2 miss (1.8% v 2.0%) at 1230. The Fed’s ‘dual mandate’ for interest rate decisions is jobs and inflation. Growth is not in their mandate and therefore does not, in general, affect rate decisions, however common sense says it is good for stocks.

Also today, White House advisor Larry Kudlow “ruled out” any currency manipulation exercise [ie selling USD], after TreasSec Mnuchin had emphasised dollar stability earlier in the week.

The reaction in the dollar was mild. A PCE miss in theory makes cuts less likely, but the MoM and YoY releases come later (next Tuesday), and in any event are too close to the decision day on Wednesday. DXY was up 0.12% and most of this was due to further 60c collapse in GBP as the new British government vowed to leave the EU ‘by any means necessary’ on Oct 31st (incidentally, the same date that ECB President Draghi leaves office, and the supposed seasonal rotation period in stocks ends. Gold was slightly up, and Oil and Yields were flat.

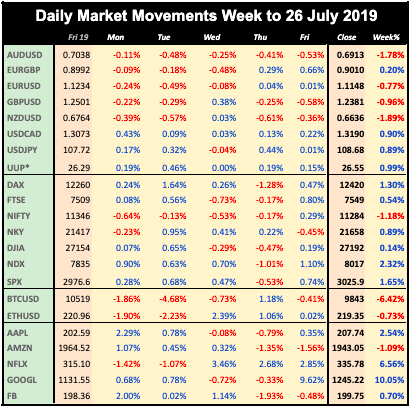

WEEKLY PRICE MOVEMENT

Earnings produced some index disconnect this week, with NDX the standout performer, up 2.32%, with GOOGL the star. NZD reversed sharply, and was the weakest currency this week. Cryptos were relatively quiet.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- First rate cut for over a decade

- Non-farm Payrolls

- UK and Japan rate decisions

- AAPL Earnings

Monday July 29

Three day China-US trade talks resume today, but there are no major European or American schedule releases. Chinese ‘BAT’ stock BIDU reports after the bell. Markets are closed in Peru and Thailand.

23:50 JPY Japan Retail Sales (Sunday)

22:45 NZD NZ Building Permits s.a. (MoM)

23:30 JPY Japan Unemp/Jobs to Applicants Ratio

23:50 JPY Japan Industrial Production (YoY)

Tuesday July 30

The first and least important rate decision this week is from Japan. DJIA defensive PG reports before the open. AAPL reports after the bell, along with AMD and NDX heavyweight GILD, and MA. Markets are closed in Morocco.

01:30 AUD Aus Building Permits (MoM)

02:00 JPY BoJ Rate Decision/Statement (e-0.1% hold)

06:00 JPY BoJ Koruda Presser

06:00 EUR Germany Gfk Consumer Confidence

09:00 EUR Eurozone Business Climate

12:00 EUR Germany CPI (e1.3% p1.5%)

12:30 USD US Core PCE MoM and YoY

13:00 USD US S&P/Case-Shiller Home Price Indices (YoY)

14:00 USD US Consumer Confidence/Pending Home Sales

20:30 WTI API Oil Stock

23:01 GBP UK GfK Consumer Confidence

Wednesday July 31

Today may set the course of the market for months. A 25bp rate cut is expected, but it is the dot-plot, the view on future rate direction that is critical. As you can see from this table, the current views are very mixed. The run-up to this decision has also shown wild swings in expectations as shown here, where the yellow bars are the likelihood of a 50bp cut (as a percentage of the two options 25bp or 50bp)

Appropriately ADP report today, about the same time as their jobs report, as do troubled ex-DJIA company GE. There is also a rate decision on BRL.

01:00 CNY China PMIs

01:30 AUD Australia CPI (QoQ e0.4% p0.3%)

06:00 EUR Germany Retail Sales

07:55 EUR Germany Unemployment Rate/Change

09:00 EUR Eurozone 19Q2 GDP (YoY e1.0% p1.2%)

09:00 EUR Eurozone Unemployment Rate

09:00 EUR Eurozone CPI (Core YoY e1.0% p1.1%)

09:30 EUR DE10Y Auction

12:15 USD US ADP Employment Change

12:30 CAD Canada GDP

13:45 USD Chicago PMI

14:30 WTI EIA Oil Stock

18:00 USD Fed Rate Decision/Statement (e2.25% p2.50%)

18:30 USD FOMC Powell Presser

22:30 AUD Aus AiG Performance of Mfg Index

Thursday August 01

The first rate decision in the Johnson premiership may produce a BoE reaction to the stronger likelihood of ‘no deal’ Brexit and the current parlous state of the pound. There is also a rate decision on CZK. Markets are closed in Switzerland, Jamaica, Barbados and Bermuda.

01:30 AUD Aus HIA New Home Sales (MoM) (time approx.)

01:45 CNY China Caixin Manufacturing PMI (e.49.6 p49.4)

07:55 EUR Germany Markit Manufacturing PMI

08:30 GBP UK Markit Manufacturing PMI

11:00 GBP BoE Rate Decision/Statement (e0.75% hold)

11:30 GBP BoE Carney speech

12:30 USD US Jobless Claims

13:30 CAD Canada Markit Manufacturing PMI

13:45 USD US Markit Manufacturing PMI

14:00 USD US ISM Manufacturing PMI (e52.0 p51.7)

23:50 JPY BoJ MPC Minutes

Friday August 02

A new month brings NFP, but as always if it’s very early, the Canadian equivalent is not concurrent. Nevertheless, for once Canadian and US Trade Balances _are_ simultaneous, so a USDCAD volatility opportunity awaits.

Oil giants CVX and XOM report before the open. Rockefeller’s Standard Oil was once the largest company in the world, these two remnants are a mere 5% of DJIA today. Markets are closed in Costa Rica, Rwanda, and Bermuda again.

01:30 AUD Aus Retail Sales

06:30 CHF Switzerland CPI

08:30 GBP UK Markit Construction PMI

09:00 EUR Eurozone Retail Sales (YoY)

12:30 USD US NFP/AHE/Unemp (NFP e170k p224k, AHE e3.2% p3.1%)

12:30 USD US Trade Balance

12:30 CAD Canada Trade Balance

14:00 USD US Michigan CSI

14:00 USD US Factory Orders (MoM)

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.