NDX worst YTD ever, DXY at 5yr highs

MY CALL THIS WEEK : BUY GBPAUD

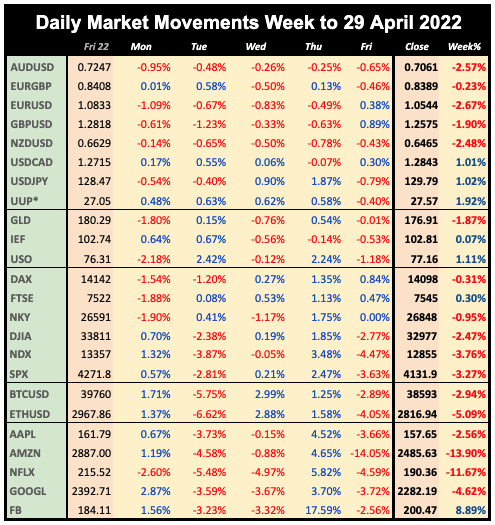

In the last week of April, continued volatility created some ominous monthly candles. NDX was down –13.3%, its largest monthly decline since 2008 and the worst start to the year ever, helped along by poor earnings from the likes of GOOGL and AMZN. A close at the low of the week and month suggests May should start off weak (more on this later) but there will then be a window to reverse from further lows. Indeed, the intra-week pattern next week could follow the same general pattern as last week, and the week before; that is early weakness leads to a mid-week bounce followed by a late sell off into Friday’s close.

WEEKLY PRICE MOVEMENT

The biggest index mover was rate-sensitive NDX for the third week, down 3.76%, nearly 14% in four weeks. The huge weight of AMZN, who missed on earnings, also affected SPX. The top forex mover was EURUSD down 2.67%. Bitcoin and Ethereum fell again, and FANGs severely underperformed, with NFLX now down 73% in six months. Once again AAPL was relatively unscathed.

Last week's EURUSD short position gained 2.67%, which means I am ahead 8.80% this year, with 9/15 (60%) wins. This week I am betting the BoE will be more hawkish than the RBA and buying GBPAUD.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK

The big index names have now reported, so the focus moves back to macro, and the key event of the week is the Fed, now expected to raise rates by 50bp on Wednesday. This is 99% priced in at CME Fedwatch, and so there ought to be a small relief rally (sell the rumor, buy the news) because it is not 75bp. As previously stated, the problem area of the Fed's dual mandate is inflation, not jobs, which are recovering steadily, meaning that NFP is not the primary focus, although there will no doubt be a short-term reaction to the upside on either a big miss or a strong beat.

Elsewhere rate hikes are also expected in Australia and the UK. The two currencies have had rather difference recent history, with AUD strong and GBP weak. Certainty on the rate hike path may normalise things. Other news is less important, with a raft of PMIs from S&P (replacing Markit) only ISM PMIs really stand out, and would have to be well wide of estimates to make a difference.

Japan is closed Monday to Thursday, and the UK is closed on Monday, meaning forex will be low volume.

CALENDAR (all times are GMT, volatile items in bold)

Monday May 2

06:00 Germany Retail Sales (p7%)

07:55 Germany S&P Mfr PMI

09:00 Eurozone Business/Consumer Confidence

13:30 Canada S&P Mfr PMI

13:45 US S&P Mfr PMI

14:00 US ISM Mfr PMI (e58.0 p57.1)

23:30 RBA Ellis speech

CALENDAR (all times are GMT, volatile items in bold)

Monday May 2

06:00 Germany Retail Sales (p7%)

07:55 Germany S&P Mfr PMI

09:00 Eurozone Business/Consumer Confidence

13:30 Canada S&P Mfr PMI

13:45 US S&P Mfr PMI

14:00 US ISM Mfr PMI (e58.0 p57.1)

23:30 RBA Ellis speech

Tuesday May 3

01:00 Aus TD Securities CPI

04:30 RBA Rate Decision/Statement (e0.25% p0.10%)

07:55 Germany Unemp

08:30 UK S&P Mfr PMI

09:00 Eurozone Unemp

13:00 ECB President Lagarde speech

14:00 US Factory Orders

16:30 BoC Rogers speech

22:30 Aus AiG Construction Index

23:00 Aus S&P Services PMI

Wednesday May 4

01:30 Aus Retail Sales (e0.5% p1.8%)

06:00 Germany Trade Balance

07:55 Germany Composite PMI

08:00 Eurozone Composite PMI

09:00 Eurozone Retail Sales (e1% p5%)

09:30 DE10Y Bond Auction

12:15 US ADP (e370k p455k)

12:30 US Trade Balance

12:30 Canada Trade Balance

13:45 US S&P Comp/Svcs PMI

14:00 US ISM Services PMI (e59.0 p58.3)

18:00 Fed Rate Decision/Statement (e1.0% p0.5%)

18:30 FOMC Press Conference

Thursday May 5

01:30 Aus Building Permits

01:30 Aus Trade Balance

01:45 China Caixin Svcs PMI

06:00 Germany Factory Orders

08:00 OPEC Meeting

10:30 ECB Lane speech

11:00 BoE Rate Decision/Statement

11:30 BoE Governor Bailey speech

12:30 US Jobless Claims

13:40 BoC Schembri speech

23:30 Tokyo CPI

Friday May 6

01:30 RBA MPC Minutes

12:30 US NFP/AHE/UnEmp (NFP e400k p431k)

12:30 Canada NFP/AHE/UnEmp (UnEmp e5.4% p5.3%)

14:00 Canada Ivey PMI