US delays some tariffs, 2/10 yield curve finally inverts, Textbook whipsaw week

Mon Aug 12

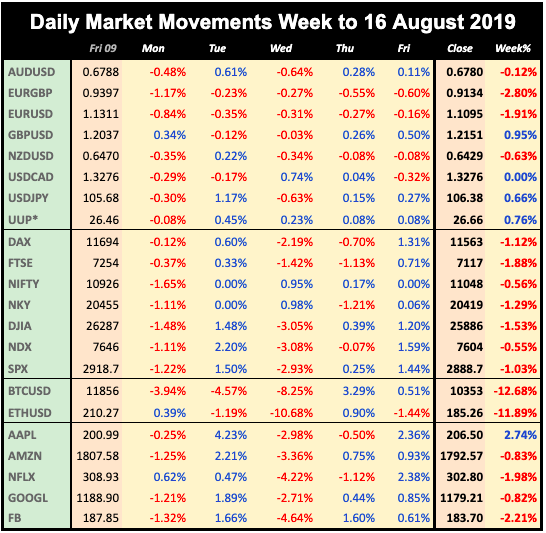

Trade war concerns continued to weigh on equities today, with SPX down 1.2%. Other world indices followed suit. The most severe move, though, was in yields, with the US 10-year falling 9bp to a new low of 1.65%, as investors moved from equities to bonds.

Risk instruments Gold and JPY were up, as was GBP, but a sharp weekend drop in EUR left DXY up 0.35%. Oil was surprisingly unaffected, and up slightly on the day.

Tuesday August 13

It’s all about the trade war, and this was proved today as President Trump announced (exactly as the US opened) that the additional tariffs on China would be delayed until December 1st. Markets reacted very strongly, as you can see from the charts above. SPX added 2% instantly, and a similar reaction was seen in all equity markets, which recovered Monday’s losses and then some.

Note what matters. DAX was up 0.6% and this was on a day that German inflation failed to beat estimates, and the ZEW Economic Sentiment estimate at 0900 came in at -44.1 (vs est -28.5), a new low.

In a textbook risk-on reaction, Gold, JPY and bonds instantly collapsed. A similar instant spike was seen in the commodity group, AUD, CAD and Oil. The effect was barely noticeable in EUR and GBP as these are not really considered to be risk on or off vis-a-vis the dollar. Both the European currencies were down on the day, coupled with the JPY move, added 0.45% to DXY.

Wednesday August 14

Before the bell today, the long-feared 2/10 yield curve inversion (the 10-year yield was lower than the 2-year) happened for the first time in 12 years. It had actually gone positive again by the time the market opened, but the move was enough to continue the whipsaw. Equity markets which all fell heavily, more than erasing Tuesday’s gains.

Everything went risk off again. Gold, JPY and bonds were sharply back up, AUD, CAD and Oil were equally sharply back down, and yields fell 12bp to a new low of 1.59%. Again the only quiet areas were EUR and GBP, the latter staying flat after the UK inflation beat at 0830.

Thursday August 15

Another bond record today, as the US 30-year bond yield fell under 2% for the first time since records began in the 1970s, and the UK equivalent fell to below 1% for the first time. Nevertheless, after the wild volatility of the last few days, equity markets took a breather. SPX was slightly up after the Retail Sales beat at 1230. The UK equivalent print at 0930 also beat, which was enough to send oversold GBP climbing, which inevitably depressed FTSE. NKY was also flat, but DAX fell.

The other components of DXY all fell, giving the basket a green candle (up 1.21%) for the day. The 10-year yield fell again, briefly touching the psychological 1.5% level. Oil was slightly down on the day, and Gold was slightly up.

Friday August 16

Markets recovered on Friday after a news report in Der Spiegel that Germany was prepared to run a budget deficit and increase debt and spending. DAX naturally rallied, and recoveries were seen in all equity markets.

A smaller risk-on more today saw Gold, JPY and bonds fall slightly, and AUD, CAD and Oil rise. Further GBP gains and EUR decline saw a flat dollar overall.

WEEKLY PRICE MOVEMENT

The GBP recovery meant FTSE was the weakest index this week, and EURGBP was the weakest currency. A pullback was seen in crypto. FANGs followed the general trend, except for AAPL which outperformed.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Jackson Hole Symposium

- Earnings season ends

- FOMC Minutes week

- Minimal other US data

Monday August 19

A quiet Monday as is often the case, although the weekend may bring market-gapping news. Chinese ‘BAT’ stock BIDU reports after the bell. Markets are closed in Colombia.

23:50 JPY Japan Imports/Exports/TB (Sunday)

09:00 EUR Eurozone CPI

Tuesday August 20

The final DJIA component HD reports before the bell, which pretty much completes the Q2 earnings season. No other US news today. Markets are closed in Hungary and Estonia.

01:30 AUD RBA Meeting Minutes

06:00 EUR Germany PPI

14:00 NZD NZ GDT Milk Index

22:00 USD Fed Quarles speech

Wednesday August 21

Another slow day for releases as markets await the FOMC minutes and Jackson Hole. Markets are closed in the Phillippines, Morocco and Bangladesh.

08:30 GBP UK PSBR

12:30 CAD Canada CPI (BoC Core YoY p2.0%)

14:00 USD US Existing Home Sales (MoM)

18:00 USD FOMC Minutes

22:00 AUD Aus Commonwealth Bank Manuf PMI

Thursday August 22

Main news of the day is the German Manufacturing PMI which has been falling for months. The annual Kansas Fed Symposium at Jackson Hole, Wyoming starts today, although it the arrival day, and only plenary speechs are expected, and probably after the market closes. There is a rate decision on IDR.

07:30 EUR Germany Markit PMIs (Manuf e43.0 p43.2)

08:00 EUR Eurozone Markit PMIs (Composite e52.1 p51.5)

11:30 EUR ECB MPC Minutes

12:30 USD US Jobless Claims

13:45 USD US Markit PMIs

23:30 JPY Japan National CPI

Friday August 23

The main day of the Jackson Hole symposium, with Fed Chair Powell speaking at 14:00. Note that Jackson Hole continues into Saturday, when the G7 Group meeting starts in France. There are therefore several possible new items over the weekend which may affect the market on Monday. Note that London is closed on Mon 26th, which may mute forex volatility.

00:00 USD Jackson Hole Symposium (all day)

12:30 CAD Canada Retail Sales (MoM, p-0.1%)

14:00 USD US New Home Sales (MoM)

14:00 USD Fed Chair Powell speech (at Jackson Hole)

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.