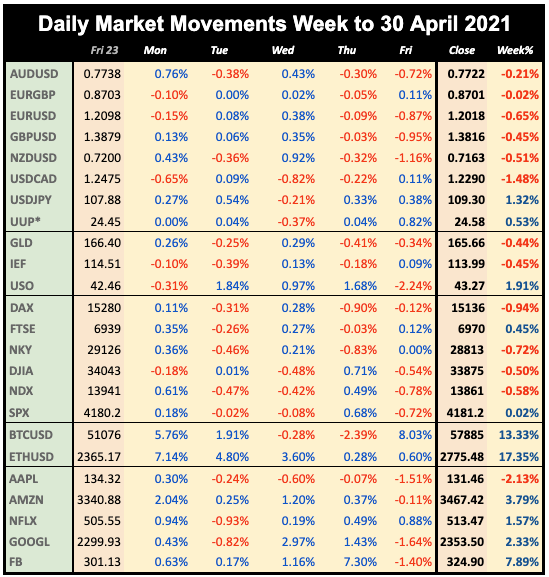

As we approach the traditional weak summer market, there were clear signs of the market being ‘toppy’. The tech giants all reported blowout earnings and revenue, but the market response for some was only moderate. When AAPL announces a 54% increase in sales, double-digit unit growth in every line, a 7% dividend increase and an additional $15 billion in buybacks, and is still down on the week, the market is telling you something. Nevertheless, the CNN Fear & Greed Index actually pulled back last week, and both SPX and NDX hit new highs but ended the week flat or down.

The Fed sounded hawkish on the economy, but dovish on action, with Jay Powell saying one great jobs report is not enough. The dollar duly fell but recovered by the end of the week. Notably CAD outperformed, following last week’s uber-hawkish BoC. Gold and bonds were also flat on the week. Notably crypto took off again.

Next week may show Powell another great jobs report, the estimate is 950k, in line with last month. It is of course also the start of ‘Sell in May’, which happened on the dot in 2019 (2020 was a special case). Otherwise we have the pause in earnings before the retailer phase, and rate decisions from the UK and Australia.

Friday’s rally continued today, although only moderately. NDX outperformed. We are also starting to see divergence between DJI and SPX. You can see from the table that results for the three indices are different each day. The dollar was slightly up although this was only really against EUR and JPY. Despite this, Gold was slightly up and Oil was slightly down. Bonds were flat on the day.

Tuesday April 27

TSLA beat on earnings Mon night, but hardly moved today. Risk appetite was weak, as markets retreated slightly and NDX underperformed. The dollar was flat with only the yen noticeably down. Gold and Oil reversed Monday’s moves and bonds were again flat. An indecision day.

Wednesday April 28

Today’s Fed meeting acknowledged the strong recovery, but Chair Powell kept up the dovish tone, saying that one good jobs report (last month’s 916k) is not enough [to start taper]. Markets reacted oddly. The strong GOOGL beat only added 3%, and both DJI and NDX fell, yet SPX managed to stay flat. The dollar fell on the Powell comments, as did yields, and Gold was up in line. Oil rose for a second day, helping CAD with it.

Thursday April 29

After a neat on US GDP (6.4%), markets were back up today, but after futures hit another ATH, there was a sudden 0.68% selloff at the open, which was recovered in the US afternoon session, meaning that DAX closed sharply (0.9%) lower. This may have been a failed front-run at Sell in May. NDX underperformed, with AAPL down despite stellar results. Notably DJIA outperformed, and copper futures hit a 10-year high of $10,000 per tonne. The dollar reversed back upwards (except against the unstoppable CAD), dragging Gold back down. Yields rose again, and Oil had a fourth green day.

Friday April 30

Another tech blowout with little to show for it. AMZN sales were up 44% with EPS smashing estimates by 65%, and remember there were no pandemic lows for the e-com giant. Yet an AH/PM 4% spike was quickly reverse, and the stock closed only 0.37% higher. Overall indices were well down, with NDX performing worst. After beats on PCE, Chicago PMI and Michigan CSI, the dollar shot up, posting its best week since early March. Gold was down in line, as was Oil after a strong run. Bonds were flat on the day.

WEEKLY PRICE MOVEMENT

The week was fairly flat overall despite tech earnings, with no index moving more than 1%. The biggest move was NKY down 0.58%. The strongest forex mover was CADJPY up 2.95% to a two-and-a-half year high. Crypto surged ahead after its reversal. FANGs outperformed NDX overall, on earnings, except for AAPL.

I sold AUDUSD last week and made 0.21%, with the continuing odd effect that I have called it right 12 out of 16 times but the cumulative 2021 profit is still only -0.58%. The extreme move in CADJPY and four weeks of reversing the most extreme pair means that I will sell that pair this week.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Non-Farm Payrolls

- UK and Aus Rate Decisions

- Earnings season pause

- First week of May

Monday May 3

The new month starts. Fed Chair Powell speaks at the ‘Just Economy’ conference. Main news is the ISM PMI. Markets are closed today in the UK and Japan.

01:00 Aus TD Securities Inflation

06:00 Germany Retail Sales (YoY e-3.1% p-9.0%)

07:55 Germany Markit Mfr PMI

13:30 Canada Markit Mfr PMI

13:45 US Markit Mfr PMI

14:00 ISM Mfr PMI (e65.0 p64.7)

18:10 Fed Williams speech

18:20 Fed Chair Powell speech

Tuesday May 4

The main news is the RBA rate decision. Markets are closed in Japan.

01:30 Aus Imports/Exports/TB (e+8000M, p7529M)

04:30 RBA Rate Decision/Statement (e0.1% hold)

08:30 UK Markit Mfr PMI

12:30 US Trade Balance

12:30 Canada Trade Balance

14:00 US Factory Orders

23:00 Aus Commonwealth Bank Svcs PMI

Wednesday May 5

The important ADP print is pitched lower than NFP this week. Markets are still closed in Japan.

01:30 Aus Building Permits

07:55 Germany Markit PMI Comp

08:00 Eurozone Markit PMI Comp

12:15 US ADP Employment Change (e808k p517k)

13:45 US Markit Svcs/Comp PMI

14:00 US ISM Svcs PMI (e73.3 p74)

23:50 BoJ MPC Minutes

Thursday May 6

Attention moves to the UK with the BoE decision.

01:45 China Caixin Svcs PMI

06:00 Germany Factory Orders s.a.

08:00 Eurozone Economic Bulletin

09:00 Eurozone Retail Sales (YoY e9.4% p1.2%)

09:00 RBA Debelle speech

11:00 BoE Rate Decision/Statement (e0.1% hold unanimous)

11:30 BoE Governor Bailey speech

12:30 US Nonfarm Productivity/Unit Labor Costs

12:30 US Jobless Claims

13:00 Fed Williams speech

Friday May 7

The first week of May ends with US and Canadian NFP, so expect USDCAD volatility.

01:30 RBA MPC Minutes

03:00 China Imports/Exports/TB (time approx.)

06:00 Germany Trade Balance/Ind Production

12:30 US NFP/AHE/UnEmp (NFP e950k p916k)

12:30 Canada NFP/AHE/UnEmp (NFP p303k)

14:00 Canada Ivey PMI

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.