Trump tariff tweets, Muted FOMC Minutes, Sterling rally on Brexit hopes

Mon Aug 19

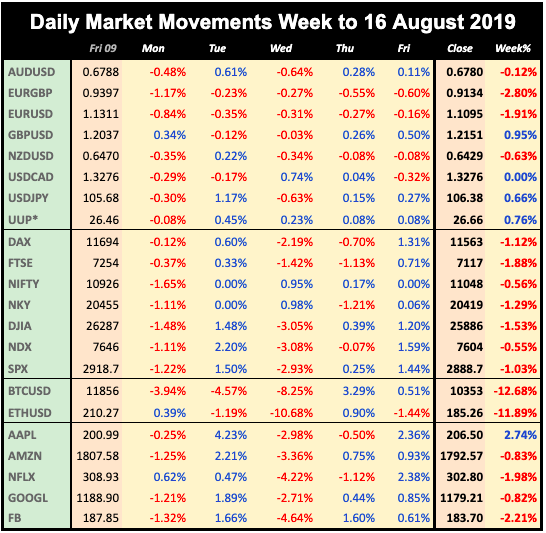

Today President Trump tweeted “we are doing very well” with the China trade talks, and there was a temporary reprieve for Huawei. This slight thaw kept markets up, and saw bond yields rise from last week’s lows. The 10-year was up 6.6bp. Equities and Oil carried on rising. The dollar was up evenly against all currencies, with CAD notably lower. Gold was down in line with the dollar, and bonds down in line with the equity move.

Tuesday August 20

As Italy’s government teetered on the brink of collapse, indices pulled back today after a three-day winning streak. All markets were down, particularly of course Italy with MIB down 1.1%. The FTSE fade was also notable as GBP joined other currencies rallying against USD. Gold and bonds rose for the same reason as yesterday as DXY gave up 0.21%. Oil was flat on the day.

Wednesday August 21

Markets recovered again today on strong earnings from retailers TGT and LOW, the former rising 20%. Indices were all up. USD was generally up (DXY +0.11%), except against CAD which outperformed after the Canadian inflation beat at 1230. Gold and bonds again moved in line, and Oil faded after a spike up following the EIA beat at 1430. The FOMC minutes were as generally expected and did not move the market.

Thursday August 22

Another directionless day as markets awaited Jackson Hole. SPX and NDX were slightly down with DJIA slightly up due to a rally in BA. DAX and EUR rallied briefly following the important German Manufacturing PMI beat at 0800, but ended the day lower. Today DXY shedded 0.05% but in reality was up generally against currencies and Gold. The reason was a strong rally in GBP up over 1% on Boris Johnson meeting European leaders and hopes of a Brexit deal.

Friday August 23

Today should have been all about Jackson Hole but it wasn’t. Fed Chair Powell’s speech was overshadowed by a curiously timed 4-tweet tirade by President Trump against China, ‘ordering’ US companies to repatriate their manufacturing jobs, and saying further tariffs would be announced later. The effect was brutal. SPX dropped 2.6% in a couple of hours, with similar moves seen around the world.

Normally, bad tariff news has no effect or even helps USD. Not today. DXY fell 0.96%, it’s largest one-day move since Jan 12, 2018 - a day of index ATHs and a three-year dollar low. This ‘equities and currency’ panic, where both fall sharply together (like FTSE and GBP on Brexit day), is always followed by a swift recovery in one or the other sooner or later.

Obviously Gold and JPY soared, but so did every other currency, as Oil and yields fell sharply with equities. Immediately after the bell the President announced a 10% increase in certain China tariffs, causing even further fading in the small Friday AH market.

WEEKLY PRICE MOVEMENT

In this risk-off week, NDX fared worst amongst indices. EURCAD was the strongest pair, up 1.75%. FANGs are more volatile than NDX as a whole, and fared worse, with NFLX the biggest loser. A very flat week from crypto, we have rarely seen BTC move less than 1% in a week.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Trade war hots up

- Germany, Japan, Eurozone inflation

- US and Canada GDP

- End of calendar month

Monday August 26

Markets will be reacting the the G7 conference, and of course President Trump’s late Friday announcements on tariffs, and his flip-flop position on this over the weekend. The Durable/Capital Goods print moved markets notably last month, maybe it will do so again. Markets are closed in the UK, so expect reduced forex volatility as London is the centre for forex.

22:45 NZD Imports/Exports/TB (Sunday)

05:00 JPY Japan Leading Economic Index

08:00 EUR Germany IFO Business Sentiment

12:30 USD Chicago Fed National Activity Index

12:30 USD Durable/ND Capital Goods (NDC e0.0% p1.5%)

23:50 JPY Japan Large Retailers' Sales

Tuesday August 27

With no particular news, markets are still likely to be dominated by the trade war. Note there are also US-Japan and US-EU trade talks this week. There is a rate decision on HUF, hold expected.

06:00 EUR Germany 19Q2 Final GDP

13:00 USD US Home/Housing Price Indices

14:00 USD US Consumer Confidence

Wednesday August 28

Another quiet day with only Germany providing planned news. There is a rate decision on ILS, hold expected.

06:00 EUR Germany Gfk Consumer Confidence Survey

09:40 EUR DE10Y Bond Auction

Thursday August 29

The heaviest news day of the week with US GDP and PCE dominating. Remember PCE is the Fed’s preferred gauge of inflation.

07:55 EUR Germany Unemployment Rate/Change

09:00 EUR Eurozone Business Climate

12:00 EUR Germany Preliminary CPI (YoY e1.3% p1.1%)

12:30 CAD Canada Current Account

12:30 USD US Jobless Claims

12:30 USD US GDP 19Q2 Prelim (Annualised e2.0% p2.1%)

12:30 USD US PCE QoQ

14:00 USD US Pending Home Sales (MoM)

22:45 NZD NZ Building Permits s.a. (MoM)

23:01 GBP UK GfK Consumer Confidence

23:30 JPY Tokyo CPI (Core YoY e0.8% p0.9%)

23:30 JPY Japan Jobs/Unemployment

23:50 JPY Japan Retail Trade

Friday August 30

The final day of the week and calendar month may bring additional volatility in equities and also in USDCAD after the GDP print.

06:00 EUR Germany Retail Sales (MoM)

09:00 EUR Eurozone Unemployment Rate

09:00 EUR Eurozone CPI (YoY e1.1% p1.0%)

12:30 USD US Personal Spending

12:30 USD US PCE MoM/YoY

12:30 CAD Canada 19Q2 Final GDP (QoQ e0.7% p0.4%)

13:45 USD Chicago PMI

14:00 USD Michigan CSI

his report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.