ECB rate cut and QE2, Sterling rallies on Brexit deal hopes, Trump postpones tariffs

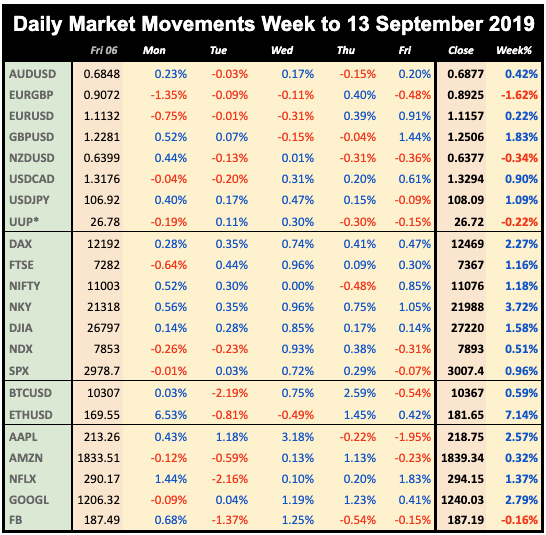

Mon Sep 09

In the absence of news, there was little action globally today, with indices more or less flat, although other markets showed a risk-on profile, with Gold, JPY and bonds firmly down, and Oil up. The exception was in the UK, where GBP rallied and of course FTSE fell, following last Friday’s success for the anti-no-deal Brexit doves, and the (accurately) predicted failure of British PM Johnson to get agreement for an election before the Brexit deadline of Oct 31. Yields were up following the Powell ’recession unlikely speech’ on Friday, a trend which continued all week.

Tuesday September 10

Another flat day in the US covering mixed action as tech fell and energy rose sharply, the latter despite a slight Oil decline. Also DJIA outperformed due to strong moves from BA and CAT. However non-US indices all rose, and Gold and JPY were slightly down in line. Other currencies were fairly flat, for once, and the real story in the US was bonds, with yields rising 11.8bp.

Wednesday September 11

A rally finally kicked in today with all markets up as investors anticipated easing in both the ECB tomorrow and the Fed next week. SPX crossed the 3,000 line, helped by a positive reception to AAPLs new cheaper iPhone and Apple TV+. Oil was up in line, helped by the EIA beat at 1530. In forex, the dollar basket was up 0.3% with all currencies (except AUD, not part of the basket) down. Yields rose more slowly today.

Thursday September 12

Today’s bold ECB moves, cutting the deposit rate and reintroducing QE caused a huge move in EUR. It initially dipped 0.88%, but as the easing moves were less than anticipated from there added 1.47%. Notably Gold, bonds and JPY spiked up and faded more in line (to the minute) with the EUR movement, as did DAX the other way (spiked down and recovered). The US inflation beat concurrent with the ECB presser was lost in the noise. As we predicted last week, President Trump tried to tweet the dollar down by contrasting today’s ECB action with the Fed next week. Overall on the day, DXY was down 0.29%.

This was enough to fade DXY by 0.29% overall, despite JPY being slightly down, the only currency to go in that direction. Indices had received a boost the night before as President Trump postponed some Chinese tariffs as a ‘gesture of goodwill’ and were comfortably up.

Friday September 13

US indices closed flat today after an early rally, whereas DAX continued up, reflecting the ECB easing, as did NKY. FTSE was down following a very strong (1.5%) rally in GBP following a reported breakthrough in the Brexit deal talks, in that the coalition Northern Irish DUP may shift their position on the Irish backstop. A further rise in EUR meant a down day for the dollar. Gold was down and Oil flat, and yields continued upwards as they have done all week.

WEEKLY PRICE MOVEMENT

NKY came out top this week in a positive week for indices, helped of course by the 1.09% fall in the yen, which also resulted in GBPJPY being the biggest forex mover, up nearly 3%. Crypto was quiet, with ETH catching up with BTC’s gain last week. FANGs were quieter than usual, but still managed to outperform the NDX index.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Fed rate cut expected

- Six more rate decisions on Thursday

- Quad-witching OpEx

- British and Canadian inflation

Monday September 16

The weekend attack on Saudi oilfields, possibly cutting their production in half may well affect Oil, and its proxies CAD and FTSE today. Markets are closed in Japan and Mexico.

02:00 CNY Retail Sales/Industrial Production

02:00 CNY NBS Press Conference

Tuesday September 17

The important German and Eurozone sentiment indicators were surveyed before Thursday’s ECB action. ECB Coeuré speaks at 1710.

01:30 AUD RBA Meeting Minutes

09:00 EUR Eurozone ZEW Economic Sentiment

09:00 EUR Germany ZEW Survey Economic Sentiment (e-38.0 p-44.1)

13:15 USD US Industrial Production (MoM)

14:00 NZD NZ GDT Milk Index

23:50 JPY Japan Imports/Exports/TB

Wednesday September 18

Today is the big day, the US rate decision. Note that the recent bond fade has pushed back the ‘priced in’ level on a 25bp cut from 90% last week to only 80%, meaning a potential stock rally to new all-time highs if the cut is delivered, unless of course Powell accompanies it with hawkish rhetoric. Also today GOOGL, FB and TWTR testify before the senate about content control. There is also a rate decision on BRL.

08:30 GBP UK CPI (YoY e1.9% p2.1%)

09:00 EUR Eurozone CPI

12:30 USD US Housing Starts/Building Permits

12:30 CAD Canada CPI (BoC Core p 2.0%)

18:00 USD Fed Rate Decision (e2.0% p2.25%)

18:30 USD Fed Chair Powell Presser

22:45 NZD NZ19Q2 Final GDP (QoQ e0.4% p0.6%)

Thursday September 19

After the Fed have made their decision, there are six more rate decisions today, as there are also decisions on NOK, IDR and ZAR. The most important is GBP, not so much for the hold, but the committee vote (the UK version of ‘dot-plot’) and its effect on the now volatile sterling. Markets are closed in Chile today.

01:30 AUD Aus NFP/UnEmp (e10k/5.3% p41.1k/5.2%)

02:00 JPY BoJ Rate Decision/Statement (e-0.1% hold)

06:00 JPY BoJ Presser

07:30 CHF SNB Rate Decision/Statement (e-0.75% hold)

08:30 GBP UK Retail Sales

11:00 GBP BoE Rate Decision/Statement (e0.75% hold)

12:30 USD US Jobless Claims

12:30 USD Philly Fed Manufacturing Survey

14:00 USD Existing Home Sales (MoM)

23:30 JPY Japan National CPI

Friday September 20

Markets will still probably be reacting to the interest rate moves but today is monthly and quarterly Opex, sometimes called quad-witching (the daily, weekly, monthly and quarterly options all expire). It’s quite important, as index future options are mainly traded quarterly. For example SPX December 19 open interest is over double that of October and November monthlies. Note also an opportunity on CAD, their rate decision was last week, but if Wednesday’s inflation moves CAD hard, Friday’s retail sales (if one is a beat and the other a miss) may well exactly reverse it.

06:00 EUR Germany PPI

08:30 GBP UK PSBR

12:30 CAD Canada Retail Sales (MoM e0.8% p0.0%)

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.