Iran retaliation muted, DJIA 29000, NFP miss halts rally

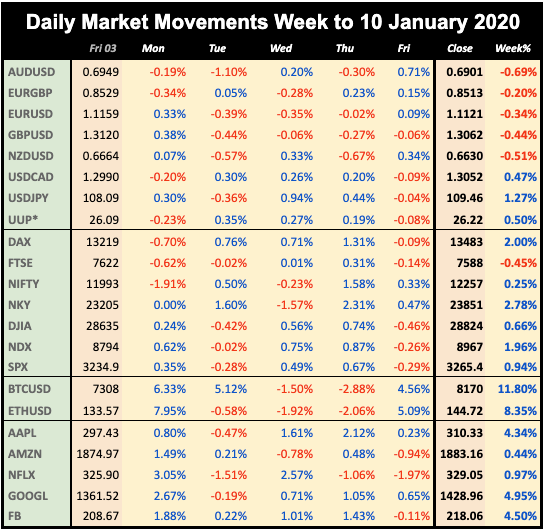

Mon Jan 6

Markets were on edge in the early part of today, continuing the sentiment from Friday, and awaiting Iran’s response to the assassination of their top general last week. However, although DAX and FTSE closed down, by the close, sentiment had recovered sufficiently to post a positive day for US indices and non-US futures. The dollar was initially sold off in London for the same reason, and did not recover by the end of the day. Gold, JPY and Bonds were of course up, but Oil faded slightly, giving back some of its huge gain on the initial action.

Tuesday January 7

Another down day for the same reasons as Monday, waiting for Iran, with all indices in the red. The dollar stayed a recovery, maybe in response to Trade Balance (1330) and Services PMI (1500) beats, which added to the beats in yesterday’s Manufacturing PMIs. However, the risk-off mood remained, with JPY, bonds and Gold all up. At the very end of the day, the Iranians did strike back, which cause a sudden move in the markets, in the risk off direction, which you can see around midnight.

Wednesday January 8

As relief unfolded that the Iranian response to the Solemaini killing was relatively muted, a few missiles at a US base with apparently no casualties, and a statement from Iran that their response was concluded, markets rallied, and risk assets and Oil fell sharply, erasing completely last Thursday’s gains. The dollar was up across the board (other than with AUD and NZD were flat/slightly up) as well, a clear change in mood, not doubt helped by the substantial beat (202k vs 150k) in the ADP jobs report.

Thursday January 9

The Iran relief factor continued into a second day, despite a series of economic misses, particularly the Chinese inflation print at 0130. All indices everywhere were up, as again was the dollar across the board. Gold was down in line, but after a 10bp move up on Wednesday, yields pulled back slightly. Oil was down although the move was much shallower than on Wednesday. Late in the day, without any fanfare, the UK finally passed its long-awaited Brexit bill.

Friday January 10

The NFP print today disappointed, coming in at 145k against the modest estimate of 164k. Futures had made a new ATH of 3288 just before the release, and then SPX (and all other indices) faded gently for the rest of the day, although DJIA briefly made a new round point high of 29000. The dollar was also down today (with only GBP going lower), and in line with equities, the haven trio were all up. Oil hardly moved, down about 30c on the day.

WEEKLY PRICE MOVEMENT

The biggest forex move in this risk-on week was unsurprisingly USDJPY, leading to the biggest index gain on the NKY. Crypto assets rallied as well, and some FANGS well-outperformed NDX generally.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Earnings season begins

- US, UK and Germany inflation

- Phase 1 deal to be signed

- Large Fed speaker roster

Monday January 13

Fed Rosengren (hawk) and Bostic (centrist) speak today, although both are non-voters. Boris Johnson’s Brexit deal, passed last Thursday in the UK’s lower house, goes to the upper House of Lords today, although the convention is that manifesto commitment bills are not challenged.

09:30 GBP UK GDP

15:30 CAD BoC Business Outlook Survey

Tuesday January 14

Earnings season opens today, with, as always the banks. Today JPM, C and WFC report before the bell. Fed Williams (dovish) and George (hawk) speak today. Only Williams has a vote.

07:00 CNY China Imports/Exports/TB

13:30 USD US CPI (MoM e0.2% p0.2%)

14:00 USD Fed's Williams speech

Wednesday January 15

The long awaited Phase 1 of the China trade deal is due to be signed today, although clearly, this is already priced in. More bank earnings today before the bell from BAC and GS, and also from DJIA component UNH. Fed Harker and Kaplan (voters) speak.

08:40 GBP BoE Saunders speech

09:30 GBP UK CPI (YoY e1.5% p1.5%)

10:00 EUR Eurozone Industrial Production

13:30 USD US PPI

16:00 USD US-China Phase One Trade Deal Signature

16:00 USD Fed Harker speech

18:00 EUR ECB Weidmann speech

Thursday January 16

A US Forex treasury report is expected today. All eyes will be on whether China is de-listed as a currency manipulator. Some smaller banks report before the bell. There are rate decisions on TRY and ZAR. US Retail Sales is the main release.

07:00 EUR Germany CPI (YoY e1.5% p1.5%)

09:30 GBP BoE Credit Conditions Survey (Q4)

12:30 EUR ECB MPC Minutes

13:30 USD US Retail Sales (Control Group MoM e0.4% p0.1%)

13:30 USD Philly Fed Manufacturing Survey

13:30 USD US Jobless Claims

15:00 USD Fed Bowman speech

Friday January 17

Fed Harker speaks again today, and there are more small bank earnings. There is a rate decision on KRW

02:00 CNY China GDP (YoY e6% p6%)

02:00 CNY China Retail Sales

09:30 GBP UK Retail Sales

10:00 EUR Eurozone CPI

13:30 USD US Building Permits/Housing Starts

14:00 USD Fed Harker speech

14:15 USD US Industrial Production (MoM) (Dec)

15:00 USD US Michigan CSI (e99.4 p99.3)

17:45 USD Fed Bowman speech

This report is published every week as an email by MatrixTrade.com - you can sign up to receive it here. This blog is supported solely by advertising, so if any of the ads interest you, please click on them. If you want notification when the blog is updated, please follow me on Twitter, Facebook, Stocktwits, TradingView or Linkedin (all open in separate windows). Details of how I compile the report are here.

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.