Powell calls for more stimulus, Whipsaw equity week, Dollar strong recovery

MY CALL THIS WEEK : BUY EURCAD

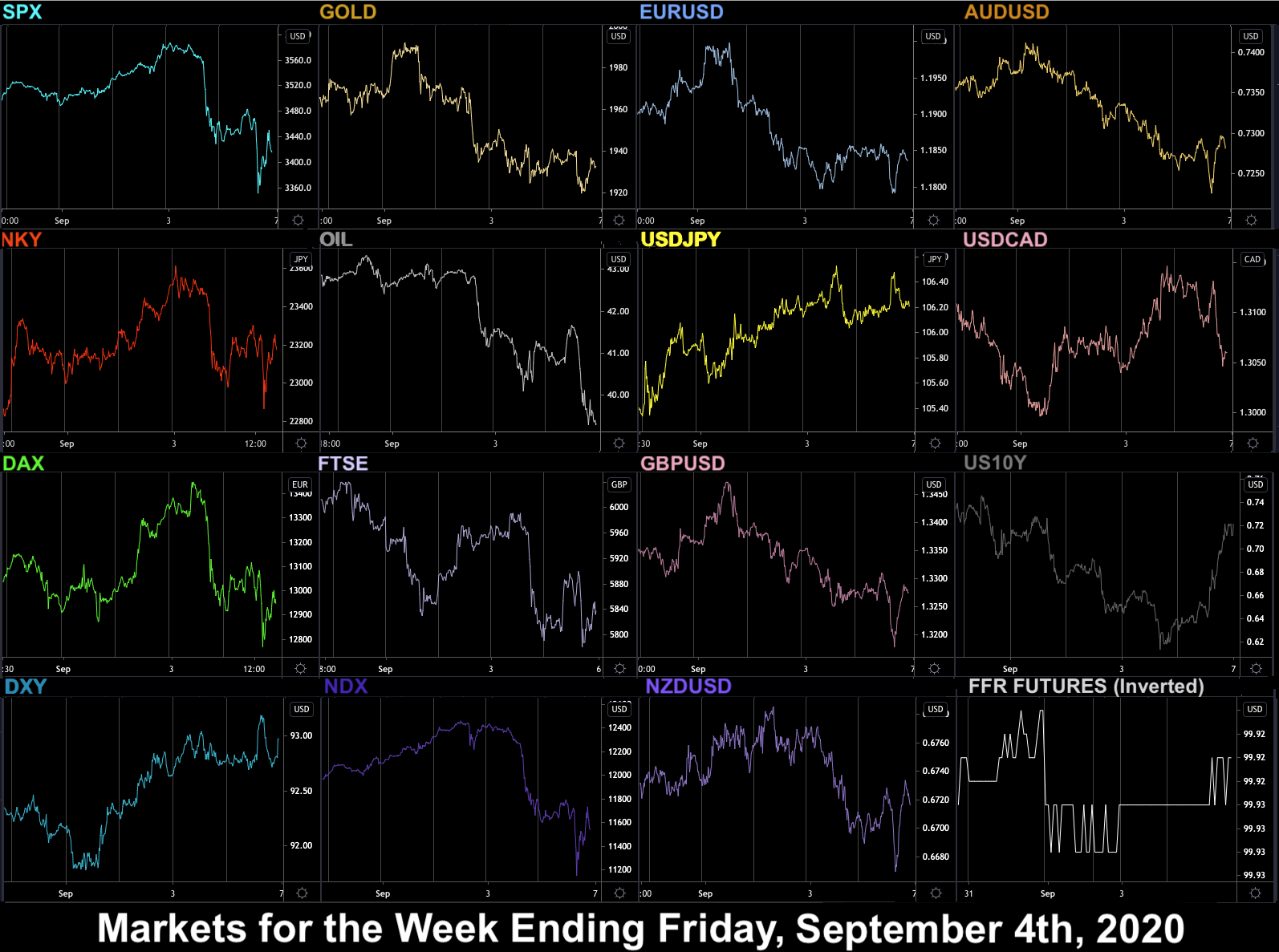

In another week where the downward pressure of COVID and election uncertainty were matched by this week’s tranche of existing QE billions, we saw whipsaw consolidation in the US, and a steady downturn in Europe, who are not beneficiaries of the Fed’s largesse. The European downturn would have been worse had not EUR and GBP faded all week against a resurgent dollar, bouncing back strongly from double bottom support last week. Gold and Oil reacted negatively to the stronger dollar.

Next week does not really promise anything different, despite the wealth of macroeconomic data. The NFP recovery is tapering, with the September estimate only two-thirds of that in August. Of possible note is the Chinese week-long mid-autumn festival around National Day which starts on Tuesday.

Concerns about a second coronavirus lockdown, the deadlock on more stimulus caused a further sharp fall in markets today (NDX managed to stay flat).

The dollar was sharply up having bottomed last week, with DXY posting its best day since July.

Gold and bonds were up and Oil down in line with equities, and JPY fell much less than other currencies.

Tuesday September 22

Fed Chair Jay Powell told Congress today that businesses hit by COVID may require further direct support. This prompted a Turnaround Tuesday today, where equity markets bounced back from the sharp sell-off, although the recovery was less effective in Europe despite weaker currencies (GBP hit a two-month low)

The dollar had a second strong day. Gold fell in line, although Oil failed to join the recovery and was slightly down. Bonds were flat on the day.

Wednesday September 23

The whipsaw consolidation continued with equities once again down, pushing through but ultimately failing to break Monday’s support low, as various Fed speakers called for additional stimulus. Oil followed them down. Dollar strength continued for a third day, with Gold reacting negatively to the dollar, not equities today. Once again, after a lively session, bonds closed flat.

Thursday September 24

A statement by Democratic leader Nancy Pelosi about being “Ready for negotiation” prompted yet another direction change as equity markets (and Oil) recovered slightly in the US, although as recovery by GBP prevented FTSE from joining the party. USD took a breather after its 3-day run, and was slightly down on the day. Despite the positive turn, Gold and Bonds were still up on the day, perhaps reflecting the dollar pause.

Friday September 25

A final rally today did not prevent stocks from closing a fourth red week, reflecting the fact that COVID is far from over. The dollar rallied again (reflected in bonds), but Gold was down in line. Oil was up on the day.

WEEKLY PRICE MOVEMENT

Whereas the US consolidated, we saw a collapse in Europe with DAX down 4.93%. The strongest forex move was AUDUSD down 3.63%. Yet another flat week for Bitcoin, but a notable pullback for ETH. FANGs outperformed NDX in strong week for tech, with AAPL the top performer.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

Monday September 28

As is often the case, today has no significant releases as go into the end of September and the US Presidential election campaign begins in earnest.

23:30 Tokyo CPI

Tuesday September 29

A thin day on news, but three Fed speakers.

09:00 Eurozone Consumer Confidence/Business Climate

12:00 Germany CPI (YoY e-0.2% p-0.1%)

13:00 US S&P/Case-Shiller Home Price Indices

13:15 Fed Williams speech

14:00 US Consumer Confidence

15:40 Fed Clarida speech

17:00 Fed Williams speech

23:50 Japan Retail Sales

Wednesday September 30

The final day of September sees the first Trump/Biden Presidential debate, and is also packed with macro news. Also it is the first day of China’s week-long National Day and Mid-Autumn Festival when markets are closed.

01:00 China PMIs

01:45 China Caixin Manufacturing PMI(Sep)

06:00 UK GDP (QoQ e-20.4% p-20.4%)

06:00 Germany Retail Sales (YoY e3.4% p4.2%)

06:00 Retail Sales (MoM)(Aug)

08:30 BoE's Haldane speech

08:55 Germany Unemployment Rate/Change

09:00 Eurozone CPI (Core YoY e0.7% p0.4%)

12:15 US ADP Employment Change (e650k p428k)

12:30 US GDP Annualised (e-31.7% p-31.7%)

12:30 US PCE

13:45 Chicago Purchasing Managers' Index(Sep)

14:00 US Pending Home Sales (MoM)(Aug)

22:30 AiG Performance of Mfg Index(Sep)

Thursday October 1

The start of a new month, with the ISM print the most important news. There are rate decisions in India and Romania today.

07:55 Germany Markit Manuf PMI(Sep)

08:30 UK Markit Manuf PMI(Sep)

09:00 Eurozone Unemployment Rate(Aug)

12:30 US PCE (MoM and YoY)

12:30 US Jobless Claims

13:30 Canada Markit Manuf PMI

13:45 US Markit Manuf PMI

14:00 US ISM Manuf PMI (e56 p56)

15:00 Fed's Williams speech

23:30 Japan Jobs/Unemployment

Friday October 2

Non-farm payrolls, as always dominates the news, as job recovery continues but at a slower pace.

01:30 Aus Retail Sales (p-4.2%)

12:30 US NFP/AHE/UnEmp (NFP e875k p1371k)

14:00 Michigan CSI

14:00 US Factory Orders (MoM)(Aug)

{kind=link}