Firm tech and general correction, Softbank ‘whale’ revealed, DJIA component change

MY CALL THIS WEEK : BUY AUDNZD

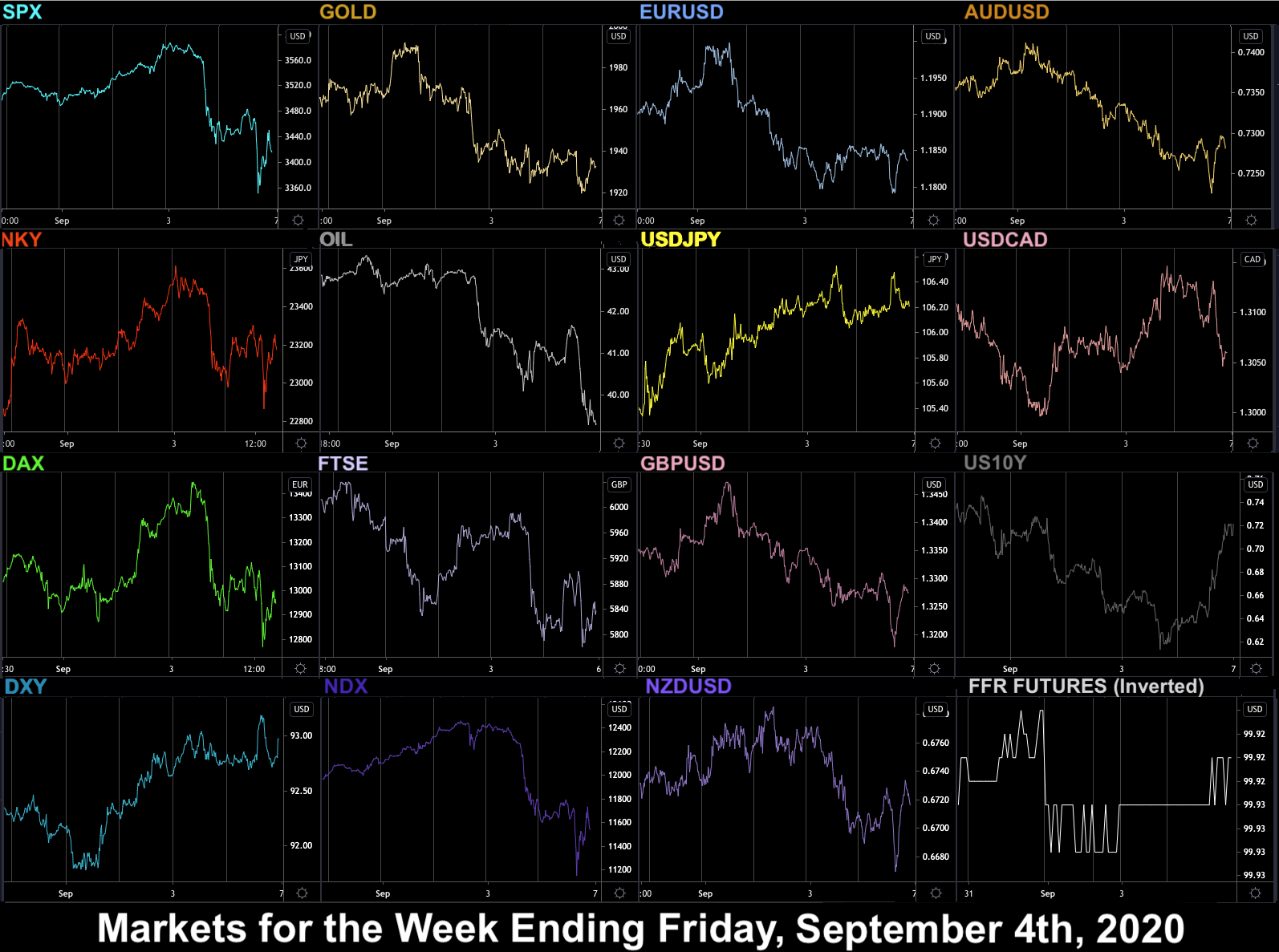

This week saw the most significant market splits (AAPL and TSLA) for years, and the market close its best August since 1986, making new all time highs in SPX and NDX. On Wednesday, NDX broke 12400, a 24% gain in two months. The next day a bubble burst, with NDX shedding 650 points, its third-largest ever point drop (and in the top 30 worst days ever). This was later confirmed to be partly due to a ‘whale’ buyer SoftBank driving up particular stocks in the tech market to extreme levels.

The DJI/NDX ratio touched 2.317 this week, a level only seen once before in the second week of March 2000. Also VIX touched its highest level since June, and notably had been rising since August 26, a rare example of index/VIX positive correlation.

There was no particular news trigger on Thursday. It was a thin news week, with only the ISM PMI (beat) on Tuesday and the ADP (miss) on Wednesday. Friday’s NFP miss may have contributed to a further fall. At the lowest point on Friday, the index was 10.3% down in two days, but still only back to the level three weeks ago.

Next week is also very thin on US macro news, with Friday’s inflation report the only print of note. We can therefore expect sentiment-driven two-way enhanced volatility which invariably follows sharp drops.

Monday August 31

It was the first day of the newly constituted DJIA today. Markets took a breather today and pulled back slightly, although NDX advanced again, and all three US indices recorded their best August since the 1980s. TSLA ramped 13% after its 5:1 stock split. Non-US indices did not join the party, both DAX and FTSE were down on stronger currencies.

Oil was down in line with the pullback. The dollar continued down, except surprisingly against JPY. However the other two haven assets move up in line with the equity fade.

Tuesday September 1

Another up day, lead by tech. AAPL was up nearly 4% (over 7% in two days), adding 0.28 points to SPX on its own, which made a new ATH. Note AAPL’s weight in SPX, at 6.89% (a market cap weighted index) is now much more than it is in DJIA (an absolute share price weighed index). Lockdown darling ZM was up 40% on earnings. Oil was up in line. DAX was flat, and again FTSE on strong sterling, touching 1.3480 for the first time in 2020,

However the RSI reading on SPX today of 83, and this fragility may be reflected in the fact that all three haven assets were up today. USD was up, after DXY touched a new 2-year low of 91.75 but this was mainly due to weak EUR after the German Manufacturing PMI miss.

Wednesday September 2

Yet another up day, but this time with DJIA outperforming NDX, with the markets shrugging off the ADP 50% jobs miss, but who can tell with jobs figures these days. DJIA stalwart KO was up 4%, whereas AAPL fell 2%. Surprisingly, Oil fell despite the EIA beat at 1530 and buoyant equities. The dollar turned up from its low, advancing across the board. Gold and JPY fell in line with equities, but yields followed the dollar.

Thursday September 3

After a quiet morning, markets fell very sharply, in a move reminiscent of Jun 11 (also a Thursday), with SPX down 3.5% and NDX nearly 5%. AAPL fell 8%. Global markets were also down, but by much less. Oil was down in line. There had been trade and PMI misses, but these were not really the trigger. In fact, nobody was surprised after the massive run up in tech stocks recently, and many commentators talked about a ‘healthy’ correction. Other asset classes were not correlated, showing this was not true risk-off. Gold and bonds were both down. The dollar was generally flat with CAD gains balancing GBP losses, and a flat EUR. Notably Bitcoin dropped 10%, its worst day since March.

Friday September 4

With very little regard to NFP (jobs slight miss but a strong beat on unemployment), the carnage momentum continued for a second day, although a late rally pared losses. For example, AAPL at one point was a further 6% down, although it managed to claw all that back and close green. TSLA was a similar story, dropping nearly 9% then recovering to close 2.8% up. Losses were still deeper in tech at the close, although the story for the week was more modest, with NDX underperforming SPX by less than 1%. Oil was down in line, more sharply in a delayed reaction (it closed at lows). This time Gold and Bonds were up in line. USD had another directionless day, closing slightly up, mainly on CAD weakness.

Today Japanese tech investor Softbank was revealed as the ‘whale’ behind the recent huge rises in tech stocks, an options strategy which is now complete.

WEEKLY PRICE MOVEMENT

NDX was the weakest index and biggest mover. AUDCAD made the largest move (1.38%) in forex. BTCUSD finally moved after weeks in the doldrums, although ETH was flat, and FANGS, in the end, roughly tracked the general NDX index.

My NZDCAD short paid off. The pair gapped down (not counted) and ended up 0.41% on the week. running total 6.32%, 15 wins out of 30. This week I am buying AUDNZD.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

- Labor day short week

- Will correction continue

- ECB and BoC rate decisions

- US, Germany, China inflation

Monday September 7

Today is Labor Day so US and Canadian markets are closed. A quiet day is expected.

03:00 China Imports/Exports/TB (time approx.)

06:00 Germany Industrial Production

23:50 Japan Q2 Final GDP (QoQ e-8.1% p-7.8%)

Tuesday September 8

A quiet news day in this quiet week. Keep watching election news.

06:00 Germany Imports/Exports/TB

09:00 Eurozone Q2 GDP (QoQ e-12.1% p-12.1%)

Wednesday September 9

A third day without significant US releases, so Canada becomes centre-stage. USDCAD is approaching 1.2950, its January low, so risk is to the upside.

00:30 Aus Westpac Consumer Confidence

01:30 China CPI (YoY e2.4% p2.7%)

14:00 BoC Rate Decision/Statement (e0.25% hold)

Thursday September 10

All eyes today on ECB President Lagarde, and the latest Eurozone stimulus plans.

01:00 Aus Consumer Inflation Expectations(Sep)

11:45 ECB Rate Decision/Statement (e0% hold)

12:30 US PPI/Jobless Claims

12:30 ECB Lagarde Presser

16:30 BoC Governor Macklem speech

Friday September 11

A portentous date, and in data, US and German inflation may be the most significant prints of the week.

06:00 UK Manuf/Industrial Production

06:00 UK GDP (MoM)(Jul)

06:00 Germany CPI (YoY e-0.1% p-0.1%)

12:30 US CPI (Core YoY e1.6% p1.6%)

18:00 Monthly Budget Statement

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.