As the month closed (Monday is a holiday), last week was the final week of May. Markets moved up on Monday, perhaps after cryptos stabilised at the weekend, and held their position in a narrow trading range all week, after Fed Clarida said he thought the current inflation level was “transitory”, and despite Fed Daly and Quarles confirming that tapering was on the agenda.

The dollar had an overall flat week, although it briefly touched a new 5-month low. Yields were slightly down but well within the recent range. Commodities on the other outperformed, with Oil and Gold touching two and four month highs respectively.

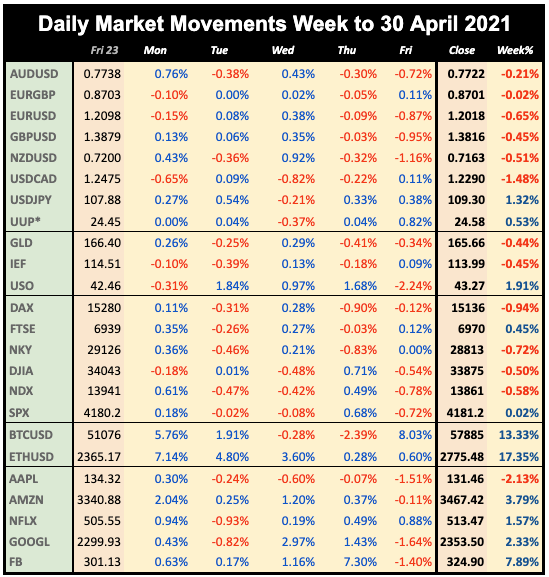

WEEKLY PRICE MOVEMENT

The biggest mover this quiet week was NKY up 2.94%. The top forex mover was NZDJPY up 2.84%. Crypto was relatively flat after recent big moves. FANGs were varied, but generally underperformed NDX.

CAD truly is unstoppable. Selling CADJPY cost me 0.73%, putting my running total back to -1.32% despite 14/20 wins. This week a different pair is the top mover, I will try reversing that, ie sell NZDJPY.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

Next week is the new month, with a four day week after Memorial Day. Markets are also closed in the UK on Monday for a Spring Bank Holid Of course NFP is the key event. The estimate at 621k is between the “good” March and April prints, and of course well above the shock miss in May. Coupled with the recent inflation trend, a good result will almost certainly be seen as a green light for QE taper, especially if the important ISM PMIs do not miss. The ADP report (on Thursday), with a slightly lower estimate, will of course be an indicator, although markets only tend to react on big ADP surprises.

The week is also packed with important non-US data, which could increase forex volatility, the risk being to the downside, given the weak dollar. Finally of course, we may see a scenario like 2019, where the market immediately reversed ‘Sell in May’.

Monday May 31

23:50 Japan Retail Trade/Industrial Production (Sunday)

01:00 China NBS PMIs (Mfg e51.1 p51.1)

12:00 Germany Prelim CPI (YoY e2.4% p2.1%)

12:30 Canada Current Account

22:30 Aus AiG Performance of Mfg Index

Tuesday June 1

01:30 Aus Building Permits

01:45 China Caixin Mfg PMI

04:30 RBA Rate Decision/Statement (e0.1% hold)

07:55 Germany UnEmp Rate/Change

07:55 Germany Markit Mfg PMI

08:30 UK Markit Mfg PMI

09:00 Eurozone CPI (Core YoY e0.9% p0.7%)

09:00 Eurozone UnEmp

10:00 OPEC Meeting

12:30 Canada GDP (QoQ e7.0% p9.6%)

13:30 Canada Markit Mfg PMI

13:45 US Markit Mfg PMI

14:00 US ISM PMI (e61.0 p 60.7)

15:00 BoE Governor Bailey speech

18:00 Fed Brainard speech

Wednesday June 2

01:30 Australia Q1 Final GDP (QoQ e2.5% p3.1%)

06:00 Germany Retail Sales (YoY e-0.3% p11.0%)

15:45 ECB Weidmann speech

18:00 Fed Beige Book

22:30 Aus AiG Performance of Construction Index

23:00 Aus Commonwealth Bank Services PMI

Thursday June 3

01:30 Aus Imports/Exports/Trade Balance (TB e8.00Bn p5.57Bn)

01:30 Aus Retail Sales (p1.1%)

01:45 China Caixin Svcs PMI

07:55 Germany Markit Comp PMI

08:00 Eurozone Markit Comp PMI

12:15 US ADP Employment Change (e545k p742k)

12:30 US Jobless Claims

13:45 US Markit Svcs/Comp PMI

14:00 ISM Svcs PMI (e62.9 p62.7)

15:00 BoE MPC Hearings (time approx.)

16:00 BoE Governor Bailey speech

23:30 Japan Overall Household Spending

Friday June 4

09:00 Eurozone Retail Sales (YoY e9.6% p12%)

12:30 US NFP/AHE/UnEmp (NFP e621k p266k)

12:30 Canada NFP/AHE/UnEmp (NFP p-207.1k)

14:00 US Factory Orders

14:00 Canada Ivey PMI