Earnings fail to lift market, dovish Fed keeps dollar weak

MY CALL THIS WEEK : SELL AUDJPY

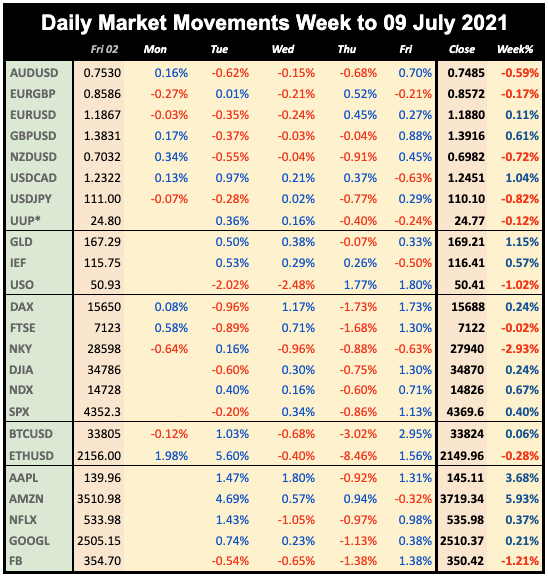

In a week where China regulation and the spread of the Delta variant provided a negative backdrop, all the main US indices – the SPX, NDX and DJI - made brief but unsustained all-time highs. Other indices fared less well with China down 10% in two session and 30% off the 2021 high, while the NKY could barely distance itself from the 2021 lows. Earnings season in the US continued the theme of significant estimate beats, but strength was generally sold. NDX fell on Wednesday despite beats from GOOGL, MSFT, and AAPL, and the AMZN revenue miss caused another drop on Friday. The FOMC was the main event of the week and provided few surprises with the Fed still signalling dovishly but making more references to taper. This helped accelerate the USD reversal to new monthly lows against all currencies and gold. The reversal also helped Oil approach the previous $75 high.

WEEKLY PRICE MOVEMENT

The biggest mover this week was NDX, down 1.01%. The top forex mover was GBPAUD up 1.53%. Crypto continued sharply upwards. FANGs, in earnings week were very variable, with AMZN down hard.

My GBPJPY made 0.41% taking my year to date profit to 4.91% and 21/29 wins. This week I am selling AUDJPY.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

A new and traditionally low volume trading month (as traders take vacations) starts on Monday. As always the new month means NFP, where the estimate, as 926k is back up is the highest since August 2020. An uptick in unemployment held off taper fears last month, but the estimate this month is once again 5.7%. A lot of smaller tech companies report earnings, but the index giants are largely done. Also next week are BoE and RBA rate decisions, and a raft of PMIs.

A new and traditionally low volume trading month (as traders take vacations) starts on Monday. As always the new month means NFP, where the estimate, as 926k is back up is the highest since August 2020. An uptick in unemployment held off taper fears last month, but the estimate this month is once again 5.7%. A lot of smaller tech companies report earnings, but the index giants are largely done. Also next week are BoE and RBA rate decisions, and a raft of PMIs.

CALENDAR

Monday August 2

22:30 Aus AiG Perf of Mfg Index (Sunday)

01:45 China Caixin Manufacturing PMI

06:00 Germany Retail Sales (p-2.4%)

07:55 Germany Markit Mfr PMI

08:30 UK Markit Mfr PMI

13:45 US Markit Mfr PMI

14:00 ISM Mfr PMI (e60.5 p60.6)

23:30 Tokyo CPI

Tuesday August 3

01:00 Aus TD Securities Inflation

01:30 Aus Building Permits

04:30 RBA Rate Decision/Statement (e0.1% hold)

13:30 Canada Markit Mfr PMI

14:00 US Factory Orders

22:30 Aus AiG Perf of Construction Index

23:00 Aus Commonwealth Bank Svcs PMI

Wednesday August 4

01:30 Aus Retail Sales (p-1.8%)

01:45 China Caixin Services PMI

07:55 Germany Markit Comp PMI

08:00 Eurozone Markit Comp PMI

09:00 Eurozone Retail Sales (p9%)

12:15 ADP Employment Change (p692k)

13:45 US Markit Comp & Svcs PMI

14:00 ISM Services PMI (e60.2 p60.1)

Thursday August 5

01:30 Aus Imports/Exports/TB (p-9.7B)

06:00 Germany Factory Orders

08:00 Eurozone Economic Bulletin

11:00 BoE Rate Decision/Statement (e0.1% hold)

11:30 BoE Governor Bailey speech

12:30 US Trade Balance

12:30 US Jobless Claims

12:30 Canada Trade Balance

23:00 RBA Governor Lowe speech

23:30 Japan Overall Household Spending

Friday August 6

01:30 RBA MPC Minutes

05:00 Japan Leading Economic Index

06:00 Germany Industrial Production

12:30 US NFP/AHE/UnEmp (NFP e926k p850k)

12:30 Canada NFP/AHE/UnEmp (NFP p-231k)

14:00 Ivey PMI