MY CALL THIS WEEK : SELL EURGBP

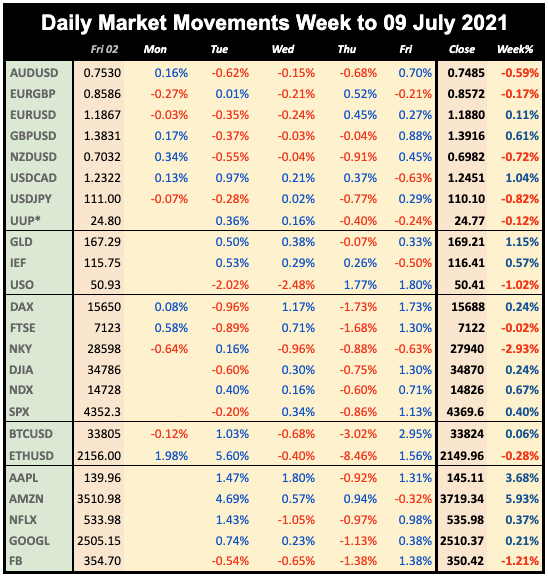

The four-day week saw stocks continued to consolidate, with a noticeable dip on Thursday, which recovered firmly on Friday, to close the week very slightly up (DJIA +0.24%, NDX +0.67%), with new SPX and NDX ATHs. The Thursday dip was influenced by falling 10-year yields, which touched February lows this week, and the ISM miss on Tuesday, but the trigger was probably the speech by Fed Bostic, who gave a very hawkish speech on Wednesday evening, saying “delaying rate rises might cause … instability”. Oil briefly touched its 2018 high on continuing OPEC uncertainty, but then pulled back from an oversold condition. The dollar had an inverted V-shaped week, slightly leading the V-shaped yield pattern. In line with the fragility of sentiment, this was largely euro and sterling strength, the latter bouncing off a three month low. Other currencies were weaker, and gold outperformed, hitting a three-week high.

WEEKLY PRICE MOVEMENT

The biggest mover this week was NKY, down 2.93% in contrast with other markets. The top forex mover was CADJPY down 1.86%. Crypto was very flat this week, with BTC probably having its flattest week for years. FANGS again outperformed NDX.

My NZDJPY short worked, making 1.25%, one of my best this year, taking my year to date profit to 4.63% and 20/26 wins. This week I am shorting EURGBP.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK (all times are GMT)

(Calendar High volatility items are in bold)

Earnings season for Q2 opens this week as always with the banks first, with EPS estimates notably lower than Q1. JPM (e3.09 p4.50) and GS (e9.41 p18.60) report Tuesday, and BAC (e.077 p0.86), WFC (e0.93 p1.05) and C (e2.01 p3.62) the day afterwards. Fed Chair Powell gives his biannual ‘Humphrey-Hawkins’ testimony to Congress. He may address the gap between stronger inflation and falling bond yields. The macro schedule is packed, with rate decisions in Canada, Japan and New Zealand, inflation from the US, UK, Eurozone and Germany. The key US print, with MoM estimated as slightly lower than last month, which may support the view that the COVID rebound figure last month was transitory. Finally, China is first out of the gate with Q2 GDP, a modest 1.3% QoQ growth is expected. Markets are closed in France for La Quatorze Juillet.

CALENDAR

Monday July 12

12:10 ECB President Lagarde speech (Sunday)

13:20 Fed Quarles speech (Sunday)

02:00 China FDI (time approx.)

Tuesday July 13

01:00 Aus HIA New Home Sales (time approx.)

02:00 China Imports/Exports/RB (time approx.)

06:00 UK Financial Stability Report

06:00 Germany CPI (e2.2% p2.1%)

12:30 US CPI (Core MoM e0.5% p0.7%)

18:00 US Monthly Budget Statement

Wednesday July 14

00:30 Aus Westpac Consumer Confidence

04:30 Japan Industrial Production

06:00 UK CPI (e2.2% p2.1%)

09:00 Eurozone Industrial Production

10:30 DE10Y Auction (time approx.)

12:30 US PPI

14:00 BoC Rate Decision/Statement (e0.25% hold)

15:15 BoC Press Conference

16:00 Fed Chair Powell H-H House Testimony

18:00 Fed Beige Book

Thursday July 15

01:00 Aus Consumer Inflation Expectations

01:30 Aus Jobs/UnEmp (Empfehlen e30k p115.2k)

02:00 China Q2 GDP (QoQ e1.3% p0.6%)

02:00 China Retail Sales (YoY e11.0% p12.4%)

06:00 UK AHE/UnEmp (UnEmp e4.7% p4.7%)

12:30 Philly Fed Mfr Survey

12:30 US Jobless Claims

13:30 Fed Chair Powell H-H Senate Testimony

Friday July 16

03:00 BoJ Rate Decision/Statement (e-0.1% hold)

06:00 BoJ Press Conference

09:00 Eurozone CPI

12:30 US Retail Sales (MoM e-0.6% p-1.3%)

14:00 Michigan CSI (e87.0 p85.5)

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.