Strong bounce back in markets

MY CALL THIS WEEK : BUY EURAUD

In a week of two-way volatility and US-EU divergence, the overall theme was of improving risk sentiment. The SPX managed to hold last Friday’s low in an early dip and has since recovered nearly 300 points (+7%). Associated markets helped the bullish case as yields fell, oil and commodities continued to drop and the USD stayed steady. Inflation expectations were revised lower. Even Bitcoin provided a tailwind as it survived the key 20k re-test and is already +20% off the lows. Pockets of weakness continued, however, especially in the eurozone. DAX made new lows on Wednesday and Thursday and the euro dropped due to poor PMIs and the likelihood that the ECB will be severely limited in any hawkish ambitions.

Developments last week suggest an interim bottom has been struck or is very close. A 5-leg decline has developed on SPX and when it completes, we should see a correction to the entire downtrend, often a 50-61% retrace. Beyond that, the view gets bearish again as the presence of trend suggests another major leg lower should unfold. Just how severe this will be hinges on a number of factors, particularly on whether or not the US can avoid a recession.

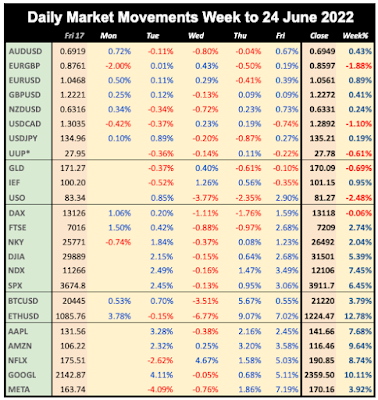

WEEKLY PRICE MOVEMENT

The biggest index mover this week was NDX, up 5.79%. The top forex mover was EURJPY up 1.08%. Crypto recovered, and FANG outperformed NDX.

My EURNZD long made 0.59% this week, meaning I am now ahead 3.68% with 12/23 (52%) wins. This week I will carry on the theme but switch to buying EURAUD.

My EURNZD long made 0.59% this week, meaning I am now ahead 3.68% with 12/23 (52%) wins. This week I will carry on the theme but switch to buying EURAUD.

Note we use Google Finance data for daily movements, listing UUP as a proxy for DXY. All references to ‘the dollar’ are based on DXY. The equity and index prices are now based on the cash close each day.

NEXT WEEK

As we close out the month, quarter and half-year, the only key US prints next week are the annualised GDP and ISM PMI. Also of interest are the PCE The big central bank event is the ECB Sintra summit (their version of Jackson Hole which is at the end of August), hence the raft of speeches on Wednesday. Markets didn't worry about the Powell testimony this week, so it is reasonable to assume there will be nothing new from the Fed Chair at Sintra. Ms Lagarde however is another story, a surprise from her could move DXY.

German inflation is still disappointingly on the increase, not helped by the fact that lagging EU tightening, a policy for all 27 member states now disadvantages the richest one, and may be a factor in SPX outperforming DAX by over 6% last week. One often overlooked release is PCE, said to be the Fed's preferred method of measuring inflation. The YoY print on Thursday is estimated to fall slightly, could this be a turning point in sentiment.

CALENDAR (all times are GMT, volatile items in bold)

Monday June 27

12:30 US Durable/ND Capital Goods Orders (DG e0.1% p0.5%)

14:00 US Pending Home Sales

18:30 ECB Pres Lagarde speech

Tuesday June 28

06:00 Germany Gfk Consumer Confidence

08:00 ECB Pres Lagarde speech

13:00 US Housing/Home Price Indices

14:00 US Consumer Confidence(Jun)

23:50 Japan Retail Sales

Wednesday June 29

01:30 Aus Retail Sales (e0.4% p0.9%)

09:00 Eurozone Business/Consumer Confidence

11:10 BoE Governor Bailey speech

12:00 Germany CPI (e8.8% p8.7%)

12:30 US PCE (QoQ)

12:30 US GDP Annualised (e-1.5% p-1.5%)

13:00 Fed Chair Powell speech

13:00 BoE Gov Bailey speech

13:00 ECB Pres Lagarde speech

15:00 ECB Pres Lagarde speech

23:50 Japan Ind Production

Thursday June 30

01:00 China PMIs (Mfr e49.6 p49.6)

06:00 UK Q1 GDP (QoQ e0.8% p0.8%)

06:00 Germany Retail Sales (p-0.4%)

07:55 Germany UnEmp

09:00 Eurozone UnEmp

12:30 US PCE (MoM and YoY) (YoY e4.7% p4.9%)

12:30 US Jobless Claims

12:30 Canada MoM GDP

13:45 Chicago PMI

22:30 Aus AiG Mfg Index

23:30 Japan Jobs/UnEmp

23:30 Tokyo CPI

23:50 Japan Tankan Mfr Index (e13 p14)

Friday July 1

01:45 China Caixin Mfr PMI

07:55 Germany S&P Mfr PMI

08:30 UK S&P Mfr PMI

09:00 Eurozone CPI (e7.8% p8.1%)

13:45 US S&P Mfr PMI

14:00 US ISM Mfr PMI (p56.1)

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.