Markets back down again

MY CALL THIS WEEK : BUY EURCAD

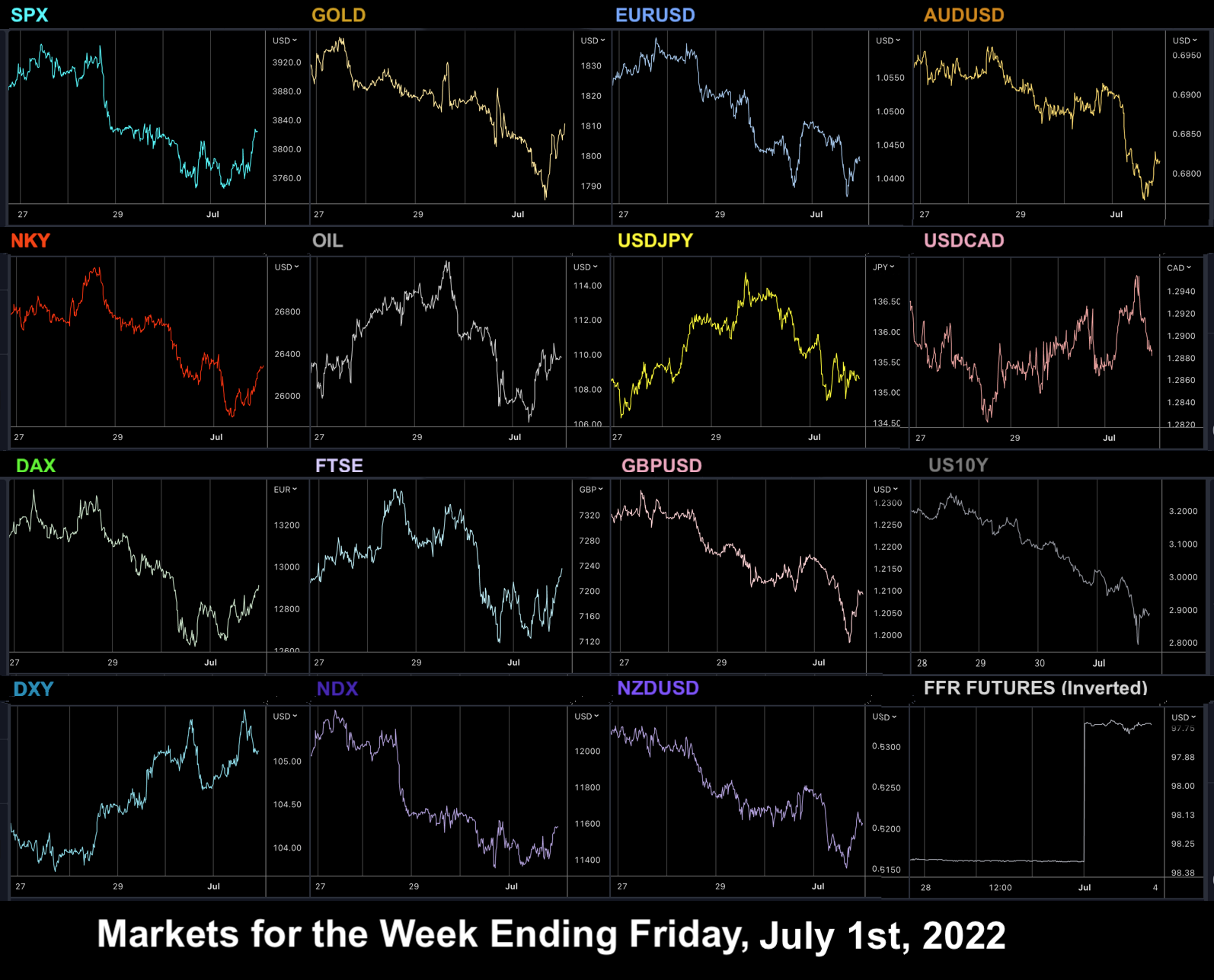

In a week where inflation concerns mixed with recession fears, the net effect was negative on stock markets as SPX and NDX retraced the late June rally and DAX maintained its relative weakness with further June lows. Currencies were mixed, but the general theme was one of USD strength as it made four higher highs and higher lows after bottoming on Monday. EURUSD re-tested the 1.035 low and looks on shaky ground as the annual central bank summit at Sintra underlined the ECB’s lack of options. ECB President Lagarde tried to strike a hawkish tone by saying that they could “move faster” depending on the data, which looked especially toothless when Spain’s CPI came in at 10.2% soon after, beating expectations by 1.4%. It begs the question: if not now, then when? Note the loose EU tone is not helping European stocks.

Inflation now looks more of a European problem than a US one as the Fed’s hiking cycle appears to be working. Long-term yields fell in the US and the 5-year forward inflation expectation rate fell to 2.08%, down from a high of 2.67% in April. Meanwhile, the 10s3s fell to 1.15% and the fall is accelerating – as inflation concerns fade, recession fears are picking up.

WEEKLY PRICE MOVEMENT

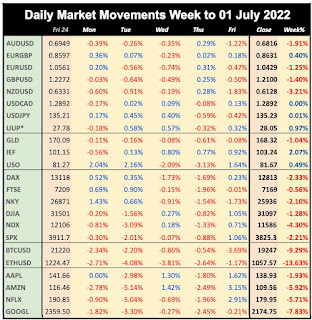

The biggest index mover this week was NDX, down 4.30%. The top forex mover was NZDUSD or NZDCAD down 3.21%. Crypto fell sharply again, and FANG underperformed NDX.

My EURAUD long made 1.12% this week, meaning I am now ahead 4.80% with 13/24 (54%) wins. This week I will carry on the theme but switch to buying EUR against the biggest riser CAD, which I think may pull back, so I will be long EURCAD.

NEXT WEEK

A new month, quarter and half year, and of course the main event is NFP. Although inflation is the primary driver of expectations of Fed action (and thus SPX pricing), the jobs report still has some effect. Traders are looking for signs that the tightening will be slowed down, and a poor report could therefore boost markets.

The week is of course foreshortened in the US (only) for Independence Day, hence why the ADP report is a day late. The only other significant event is the RBA rate decision, where a 50bp hike is expected, and may reverse the AUD trend, which is now trading at a one-year low. There are several trade balance and PMI reports but as you know, these have much less effect on markets than central bank actions.

CALENDAR (all times are GMT, volatile items in bold)

Monday, July 4

01:00 Aus TD Securities Inflation

01:30 Aus Building Permits

06:00 Germany Trade Balance

13:30 Canada S&P Mfr PMI

14:30 BoC Business Outlook Survey

22:30 Aus AiG Construction Index

23:00 Aus S&P Svcs PMI

Tuesday, July 5

01:45 China Caixin Svcs PMI

04:30 RBA Rate Decision/Statement (e1.35% p0.85%)

07:55 Germany S&P Comp PMI

08:00 Eurozone S&P Comp PMI

08:30 UK S&P Comp PMI

09:30 UK Financial Stability Report

14:00 US Factory Orders

16:30 BoE Tenreyro speech

Wednesday, July 6

06:00 Germany Factory Orders

08:10 BoE Pill speech

09:00 EC Growth Forecasts

09:00 Eurozone Retail Sales (e5.4% p3.9%)

09:30 DE10Y Bond Auction

13:45 US S&P Comp & Svcs PMI

14:00 ISM Svcs PMI (e55.7 p55.9)

18:00 FOMC Minutes

Thursday, July 7

01:30 Aus Imports/Exports/TB

11:30 ECB MPC Minutes

12:15 US ADP (e200k p128k)

12:30 US Trade Balance

12:30 US Jobless Claims

12:30 Canada Trade Balance

14:00 Canada Ivey PMI

23:50 Japan Current Account

Friday, July 8

12:30 US NFP/AHE/UnEmp (NFP e250k p390k)

12:30 Canada NFP/AHE/UnEmp (UE e5.2% p5.1%)

No comments:

Post a Comment

Please leave a comment. They are moderated and spam (links to your site) will not be published.